How to Apply for SEIS/EIS Advance Assurance: Step-by-Step Guide (2025)

In 2026, the cleanest way to apply for SEIS/EIS advance assurance is to prepare a tight, investor-ready pack and submit it via HMRC’s online service. Expect follow-up questions on eligibility, share rights, group structure, and risk-to-capital. Treat assurance as a signalling document for investors and a rehearsal for your later compliance filing (SEIS1/EIS1).

If you’re raising your first institutional pound in the UK, SEIS/EIS advance assurance is the quiet document that unlocks the louder conversation. It doesn’t promise capital, but it oils the hinges: angels move faster, round dynamics improve, and your legal/finance workflow becomes less brittle. In 2025, when investors are choosier and diligence cycles are longer, coming to the table already knowing what SEIS advance assurance is and what EIS advance assurance isn’t just tidy; it’s tactical.

Advance assurance is HMRC’s non-binding view that a proposed share issue is likely to qualify for a venture capital scheme (SEIS or EIS), based on the facts you present. It helps you show prospective investors that your round is structured to support their tax relief and aligns with the HMRC approval process that founders navigate before issuing shares. In this guide, you’ll get a complete roadmap: how to apply for SEIS/EIS advance assurance, the exact documentation, the online form, what HMRC looks for, where applications stall, and crisp answers to the questions founders and angels ask most. We’ll also explain how to get EIS advance assurance if you’re already past the earliest stage, and how to sequence SEIS then EIS so you don’t trip over the rules later.

If you prefer a ready-made path, Undo Capital packages the entire SEIS/EIS advance assurance workflow, documents, sequencing, and filings, so you can focus on the raise rather than the paperwork.

What Is SEIS/EIS Advance Assurance?

SEIS/EIS advance assurance is HMRC’s non-statutory, discretionary opinion on whether your proposed share issue would likely qualify under the UK’s venture capital schemes, based on the specific facts you submit. It’s evidence for investors, not a guarantee of tax relief, and HMRC can ask for further information or decline to opine where facts are unclear.

SEIS vs EIS advance assurance: What’s the difference? Both follow the same online process, but they test against different scheme rules (age of company, asset and headcount thresholds, allowable activities, and funding limits). You can apply for one or both; what matters is that each proposed investment you want covered is supported by a separate set of facts.

Why Advance Assurance Matters for Startups

- Investor confidence. Many angels and funds condition term sheets or escrow on seeing HMRC’s letter. It signals that your round has been structured with care and that you’ve documented eligibility (including the “risk to capital” condition).

- Eligibility clarity before you raise. If HMRC flags problems (non-qualifying trade, share rights, group structure), you’d rather fix them pre-raise than post-close. The advance assurance letter is also the reference point you’ll cite in your later compliance statement (SEIS1/EIS1) after you issue the shares.

- Is it mandatory? No. HMRC’s advance assurance service is optional and discretionary. But in practice, most early-stage rounds are easier and faster when you have it, especially when investors are scrutinising startup funding compliance up front.

- Common misconception: “Does advanced SEIS assurance mean EIS as well?” No, SEIS and EIS are distinct. You usually need separate applications (or at least separate coverage for each proposed investment).

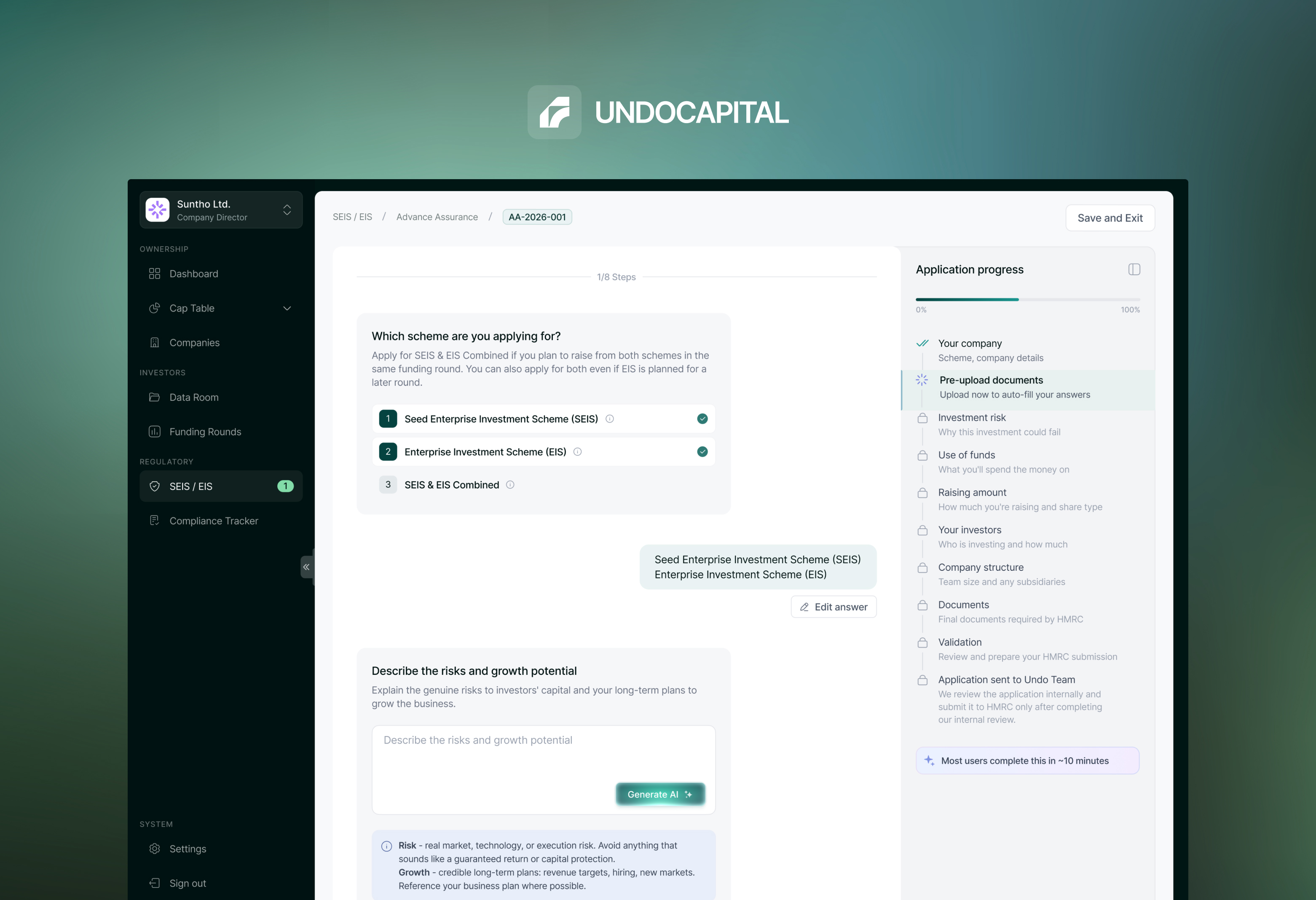

Operational Path to SEIS/EIS Advance Assurance

Checklist before applying (what needs to be done before assurance for SEIS/EIS):

- Confirm your scheme fit (SEIS for earliest-stage; EIS for later growth).

- Map your structure (subsidiaries, parent) to ensure a qualifying status.

- Draft your business plan and financial forecasts; HMRC requires them.

- Assemble your register of members, latest accounts (if available), memorandum and articles, and draft fundraising documents (IM/deck/ASA/subscription).

- Prepare details of prospective investors or evidence of platform/fund manager engagement (HMRC asks for this, especially for first-time users of the schemes).

- Articulate how you meet risk to capital (growth & development intent; real capital at risk).

HMRC explicitly lists what you’ll need: the amount you plan to raise, plans & forecasts, latest accounts, group usage of funds, trading activities, and spend by activity, M&A, register of members, investor materials, any shareholder agreements, and evidence you meet risk-to-capital, plus details of potential investors or engagement with a platform/fund manager.

Step 1: Prepare Your Documents

Gather:

- Business plan & 3-year forecasts (assumptions clear and tied to use of proceeds).

- Company information: incorporation details, UTR, SIC code(s), ownership (cap table) and an up-to-date register of members.

- Draft legal docs for the round (ASA/subscription agreement, term sheet, any shareholders’ agreement).

- Investor evidence: names/addresses of prospective direct investors, or acceptance/engagement letters from a crowdfunding platform or fund manager, if applicable.

- Articles of association (with any planned changes).

- Explanation of how you meet risk-to-capital (growth intent; no risk-reduction arrangements).

1) Business plan & forecasts (and how they tie to the use of proceeds)

Your plan doesn’t need to be a coffee-table book. It needs to make three things obvious:

- What you sell, to whom, and why it’s defensible. Open with the problem, your product, the buying motion, and the two or three levers that will drive growth (distribution, unit economics, regulatory angle, IP, or network effects).

- How cash turns into milestones. Spell out exactly what the SEIS/EIS money buys, hires, product sprints, regulatory clearances, pilots, and go-to-market. Then show the milestone dates that those spends unlock.

- A forecast that reconciles. Keep it for three years, monthly for Year 1, quarterly thereafter. Anchor assumptions (pricing, conversion, churn, ramp time) and include a simple sensitivity: base vs. downside.

Make the link explicit. Add a one-page “Use of Proceeds Map” that ties every pound you’re raising to a budget line and a milestone. If you say £180k goes to engineering, the headcount plan should show the roles, start dates, and salaries; the forecast should show the burn impact; and the hiring plan should list who you’re targeting and when. The case officer shouldn’t have to infer.

Founder tip: If you’re running a platform-assisted raise, include the acceptance note or dashboard PDF. Undo Capital can generate a simple investor-evidence sheet that collates names/addresses and intended SEIS/EIS split in one place.

2) Company pack (the “who we are” proof)

This is the paperwork that says you are who you say you are, and that your cap table is real, current, and consistent.

- Incorporation details & SIC codes. Include the certificate of incorporation and current SICs. If your SICs don’t reflect your actual trade yet, add a note explaining the planned change on the next confirmation statement.

- Register of members + cap table. The register is the legal record; the cap table is the model. They must match. Date both, include share classes and counts, and show all historic allotments. If you plan to expand the option pool before the round, show that explicitly in a pre- vs. post-money view.

- Latest accounts (if available). Micro-entities still help: balance sheet + notes. If you’re pre-revenue, your narrative should explain burn, creditors, and any director loans.

- Articles of association (current). Put the exact version that’s in force today. If you’ll amend them at close, park those changes in the “draft round docs” (below), not here.

Founder tip: Start the company pack with a one-page “Contents & Cross-Checks” sheet that lists each exhibit and the page where a case officer finds: (a) share classes outstanding, (b) current directors, (c) trading status, (d) group structure (if any).

3) Draft round documents (what investors will actually sign)

HMRC is looking for full-risk ordinary equity with no features that materially protect investor capital. Keep documents clean and consistent.

- ASA/subscription agreement. If you’re using an ASA, make sure the conversion mechanics don’t create disguised protection (e.g., guaranteed minimum returns). If you’re doing a priced round, the subscription should match the share rights you describe in the plan.

- Term sheet. State the instrument, amount, and any conditions precedent. If you’re raising SEIS, then EIS, put the sequence and target amounts in black and white.

- Proposed changes to articles. House them in a marked-up draft. Keep anything resembling redemption, capital protection, or preferential return out of the share class investors will buy under the scheme.

- Shareholders’ agreement (if any). Voting and information rights are fine. Ratchets, put/call options that limit downside, or early-exit arrangements are red flags; remove them or put them outside the SEIS/EIS tranche.

Founder tip: Add a two-column “Share Rights Snapshot” table to your cover note: left = right (e.g., dividends, pre-emption, drag/tag); right = whether it applies to the qualifying ordinary shares (Yes/No) with a page reference to the clause.

4) Investor evidence (the thing most teams forget)

For first-time users of the schemes, HMRC usually expects proof that real investors are engaged. You have options:

- Direct angles. List names and correspondence addresses (even if provisional), ticket sizes if available, and whether they’re claiming SEIS or EIS.

- Platform/fund manager. Include acceptance or engagement letters, or a screenshot/PDF of the platform dashboard confirming your campaign is approved (with company name visible).

- Lead-investor email. A simple letter of intent on the investor’s letterhead (or an email saved to PDF) stating interest, estimated ticket, and that they expect to rely on SEIS/EIS relief is useful.

Founder tip: Label this document “Prospective Investors, Evidence & Contacts (SEIS/EIS)” and add a short paragraph up top explaining your pipeline and timelines. You’re not proving the round is closed; you’re proving it’s real.

5) Risk-to-capital memo (make the commercial story explicit)

This isn’t a place for slogans. It’s where you demonstrate two things: (1) long-term growth and development is your objective; and (2) investor capital is genuinely at risk (no arrangements to reduce downside).

A simple, effective structure:

- Business model & market path. What you’re building, target segment, and the steps to scale (e.g., regulatory approvals, channel partnerships, product sprints, hires).

- Use of funds → growth. Tie the raise to specific growth activities (team, product, market development). State numbers and dates.

- Why is capital at risk? Commercial uncertainties (adoption, competition, execution), absence of guarantees, and confirmation that there are no arrangements to protect capital or deliver a pre-planned exit.

- No disqualifying features. Confirm shares are ordinary, fully at risk; no redemption rights; no preferential return of capital; no linked loans or reciprocal arrangements.

- Time horizon. Emphasise that the company intends to grow and develop over the long term; this isn’t a vehicle for short-term tax-driven recycling.

Founder tip: End the memo with a one-line certification from a director: “I confirm the facts above are accurate and there are no arrangements to secure or protect investor capital.”

Step 2: Complete the HMRC Application

Use HMRC’s “Apply for advance assurance on a venture capital scheme” online service (Government Gateway). Agents can apply with authority; expect to include the pack above, plus investor evidence.

Where to send the EIS/SEIS advance assurance form? Online via HMRC’s service (“Start now”).

Or you can let the Undo Capital platform handle it: it checks your eligibility, validates your details against HMRC criteria, flags risks automatically, prepares the application and submits it for you.

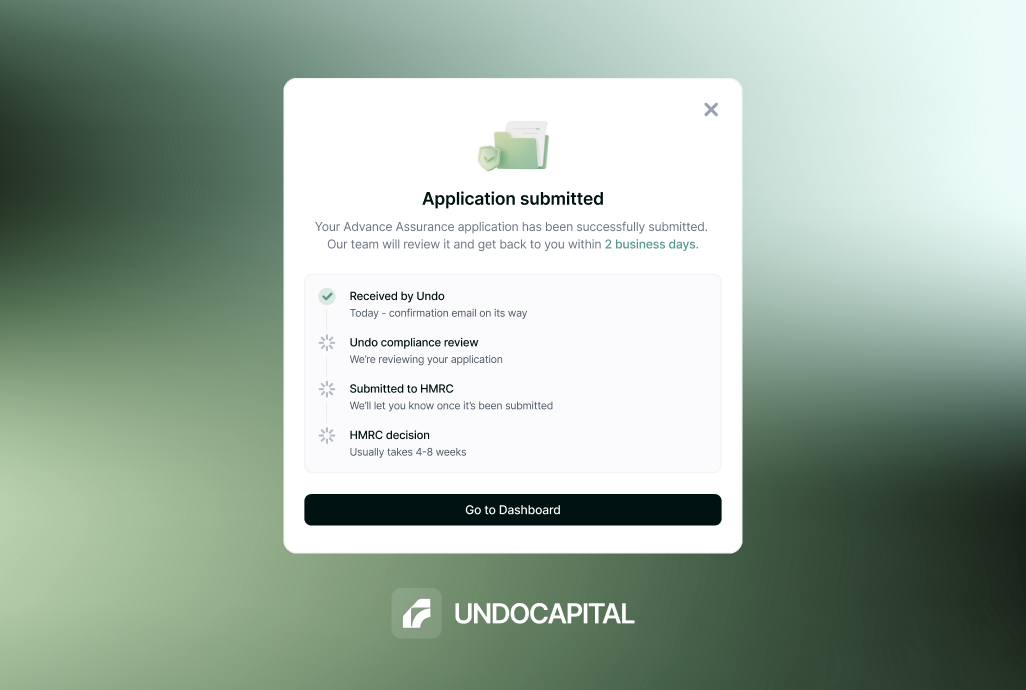

Step 3: Submit to HMRC

Submit one application per proposed investment, making the SEIS→EIS sequencing explicit in your narrative and cap-table timing. Check numbers reconcile across plan, forecasts, and use of proceeds.

If you use Undo Capital EIS/SEIS advance assurance form, we handle the entire submission process on your behalf, so there is no need for you to submit anything directly to HMRC.

Step 4: HMRC Review & Communication

HMRC reviews eligibility and may ask for clarifications (trade, share rights, investor evidence, group). They will contact you when they make a decision; there’s no published service-level. Respond quickly to RFIs.

How can I check if I have SEIS advance assurance? You’ll receive HMRC’s statement/letter if granted; for case queries, use the contact route HMRC provides.

Step 5: Receive Your Letter

If successful, HMRC issues a statement you can show investors. After you issue shares, file your compliance statement, SEIS1 or EIS1, then issue SEIS3/EIS3 certificates once authorised. (If facts change materially between assurance and compliance, tell HMRC; otherwise, the assurance no longer applies.)

How Long Does SEIS/EIS Advance Assurance Take?

There’s no fixed published timeline; HMRC simply states it will contact you when a decision is made and may request additional information. Sensible founders build several weeks of runway into the plan and avoid the March/April crunch.

For context, HMRC’s 2025 statistics show thousands of advance assurance requests each year and robust approval rates (as of March 2025, ~76% of EIS advance assurance applications had been approved; ~85% for SEIS), which is encouraging—provided the submission is complete and consistent.

What speeds this process:

- A self-contained, coherent pack. Numbers align across your business plan, forecasts, and use of proceeds; your articles and draft subscription/ASA reflect the same share rights you describe.

- Prospective investors named. First-time scheme users who include real investors (or a platform/fund manager’s engagement) typically avoid the “please provide investor details” loop.

- A crisp risk-to-capital memo. Spell out growth and development (hires, product, market) and the absence of risk-reduction features.

- One application per proposed investment. If you’re doing SEIS, then EIS, keep them logically sequenced and separately explained.

Bottom line: how long does SEIS/EIS advance assurance take depends far more on the quality and stability of your submission than the date on the calendar. You can’t force a deadline, but you can present a file that reads cleanly, anticipates the obvious questions, and lets the caseworker say “yes” without reaching for another email.

Fast responses to HMRC. Treat any follow-up as time-critical; a same-day or next-day reply keeps momentum.

How Long Does SEIS/EIS Advance Assurance Last?

There’s no statutory “expiry date.” Advance assurance is based on the facts you submitted and remains useful so long as those facts haven’t changed. HMRC’s own guidance tells companies to disclose any changes since the application when filing the compliance statement; if material facts change, the assurance will no longer apply to the modified proposal. In short: no fixed shelf life, but keep the facts aligned, or refresh.

SEIS vs EIS Advance Assurance: Key Differences

Practical sequencing rule: Start with SEIS eligibility (where you qualify), then move to EIS eligibility. The EIS guidance explicitly notes that once you issue EIS shares, you cannot subsequently issue SEIS shares.

If you’d rather spend time with investors than appendices, Undo Capital centralises SEIS/EIS advance assurance, investor agreements, share issue, and filings, so the SEIS→EIS sequence stays clean from draft to SEIS3/EIS3.

Common Mistakes to Avoid When Applying: Essential pitfalls that delay or derail SEIS/EIS approval

FAQs

Do I need separate advance assurance for SEIS and EIS?

Yes. SEIS and EIS are separate schemes. If you plan to raise under both, you’ll need distinct coverage. Undo Capital makes it easy by guiding you through the correct sequence (SEIS first, then EIS).

How long does SEIS/EIS advance assurance take?

Timelines vary depending on HMRC’s workload. While HMRC quotes 6–8 weeks, at Undo Capital we usually see results in less than a week on average. Our automated checks, document preparation, and application tracking reduce delays and help you avoid unnecessary back-and-forth.

Is advance assurance mandatory before raising investment?

Legally, no. But in practice, most investors want to see it. It gives them confidence that they’ll qualify for tax reliefs. Undo Capital helps you secure this assurance upfront so fundraising conversations move faster.

How long is advance assurance valid?

It doesn’t “expire” on a set date. It’s valid as long as your facts and structure don’t materially change. If anything does change, Undo Capital flags this for you before you file compliance.

What happens if HMRC rejects my advance assurance?

HMRC will explain why. Undo Capital helps you understand the reasons, re-work your structure or documents if needed, and reapply quickly — so you don’t lose investor momentum.

References

Disclosure Notice: This communication is issued by Undo Capital Limited (“Undo Capital”) and is provided strictly for informational purposes only. It contains general information and should not be relied upon as accounting, business, financial, investment, legal, tax, or other professional advice. Undo Capital is not regulated by the Financial Conduct Authority (FCA) and does not provide investment, financial, or tax advice. Our services are designed to assist startups and businesses with company formation, legal agreements, and funding-related documentation. Nothing in this communication constitutes, or should be construed as, a recommendation, offer, or solicitation to purchase or sell any security or financial instrument.

Participation in startups and early-stage enterprises involves significant risk. Such investments may be illiquid, may not generate dividends, may be subject to dilution, and may result in the total loss of invested capital. Any decisions or actions that may affect your business or personal interests should be taken only after seeking advice from suitably qualified professional advisors, and should form part of a balanced and diversified portfolio. This communication may contain links to third-party websites. The inclusion of such links does not imply endorsement, approval, investigation, or verification by Undo Capital. We accept no responsibility or liability for the content, accuracy, or use of information contained on any third-party websites.

Latest articles

%20Explained%20for%20UK%20Founders.jpg)

Share Incentive Plan (SIP) Explained for UK Founders

S431 Election Explained: What UK Founders Must Do When Issuing Shares to Employees