SEIS/EIS Eligibility Criteria Explained for Founders

If you’re building in the UK, there’s a moment when the pitch deck, the roadmap, and the early believers converge, and all that separates talk from capital is clarity. The UK’s SEIS/EIS eligibility for startups is the bridge. These two venture capital tax relief schemes were designed to reward risk-taking and keep innovation close to home. For founders, they broaden the pool of angels willing to back a first or second act; for investors, they soften the downside and amplify the upside. Understanding the SEIS eligibility criteria and EIS eligibility criteria, before you draft a single term sheet, is the single most useful hour you’ll spend this quarter. (And yes, advance assurance comes next.)

At the end of this guide, you’ll find a straight-talk checklist and a compact FAQ. Along the way, where it’s helpful, we’ll point out how Undo Capital automates the grind, from fast eligibility checks to SEIS1/EIS1 filings, so you can move from intent to investment without losing a week to paperwork.

What Is SEIS and EIS Eligibility?

SEIS eligibility means your company, trade, investors, and share issue meet HMRC’s rules for the Seed Enterprise Investment Scheme, typically very young companies (≤3 years trading), modest assets (≤£350k), <25 employees, qualifying trades, and proper use of funds within 3 years. EIS eligibility applies to slightly later companies (generally ≤7 years from first sale; extended for KICs), with higher asset/employee thresholds and different funding caps and spend windows.

Put simply: who qualifies for SEIS/EIS? Early-stage UK companies with growth intent, carrying on qualifying trades, issuing new ordinary shares, and meeting the risk-to-capital condition, plus investors who are individuals, not “connected,” and who hold shares for the minimum period.

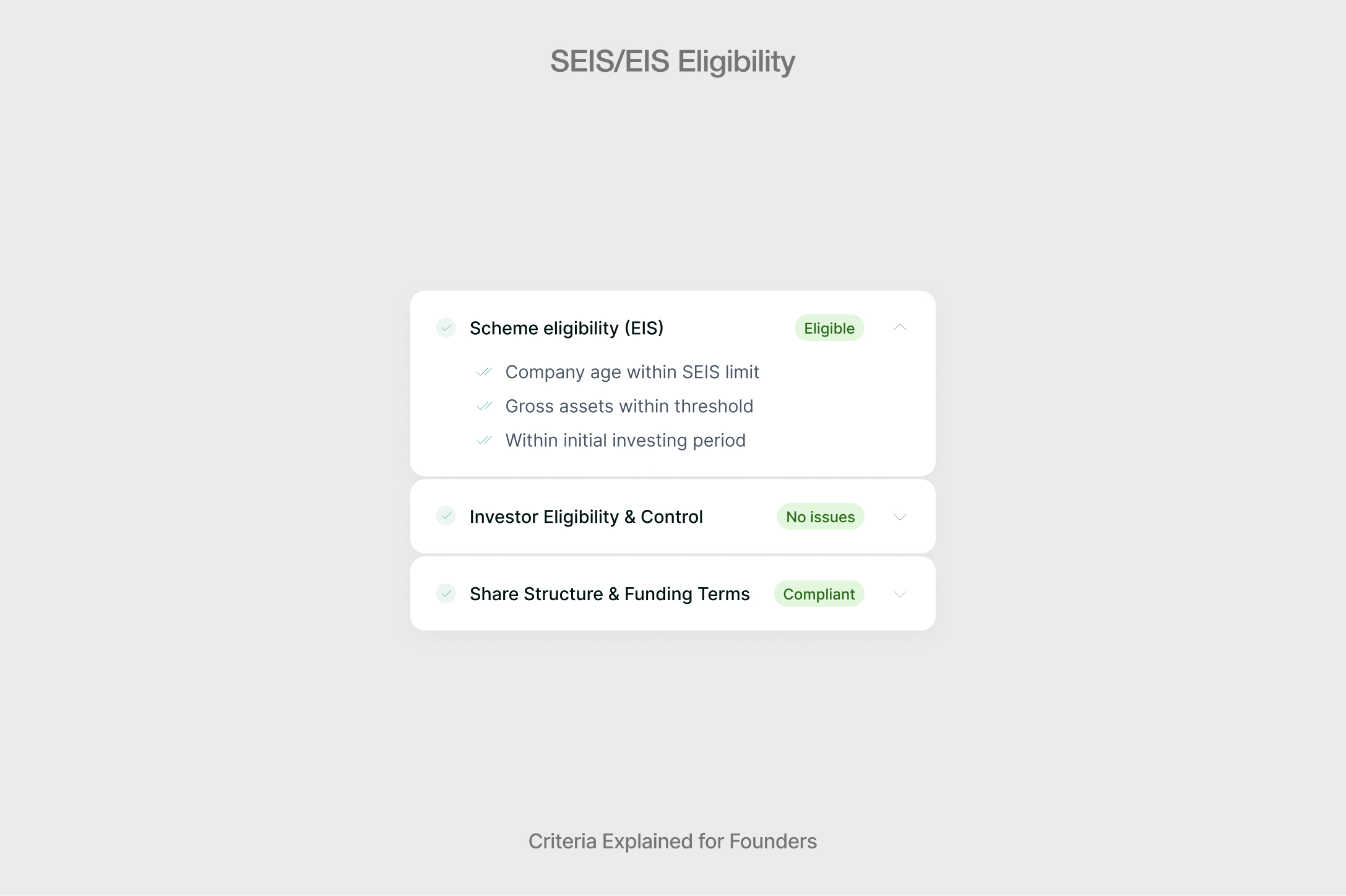

SEIS Eligibility Criteria for UK Startups

The SEIS requirements in the UK are precise but intelligible. Think age, size, trade, how you spend the money, and how you structure the round.

SEIS Company Conditions

- Age & “new trade”: SEIS supports new qualifying trades up to 3 years old at the time of investment. If your company already trades, that trade must not have been carried on for more than 3 years (including by a prior owner who transferred it in).

- Gross assets: ≤£350,000 immediately before the share issue.

- Employees: <25 full-time equivalent employees at the time of the investment.

- Funding cap: £250,000 total under SEIS per company (lifetime).

- Unquoted: You must be unquoted, no shares listed on a recognised stock exchange (AIM and AQSE Growth are not recognised; AQSE Main Market is).

- Qualifying shares: Newly issued, full-risk ordinary shares, paid in cash, no redemption or preferential rights that protect the investor. (See HMRC VCM for share requirements.)

SEIS Qualifying Trades

- Your trade must be commercial and with a view to profit.

- You must not carry on excluded activities to a “substantial” extent. HMRC interprets “substantial” as generally >20% by a reasonable measure (turnover, assets, time).

- Common exclusions include financial activities, property development, energy generation benefiting from certain subsidies, and legal/accountancy services.

Use of Funds & Timing

- SEIS money must be used within 3 years for a qualifying business activity: carrying on a qualifying trade, preparing to trade, or R&D expected to lead to one. You cannot use SEIS to buy shares in another company, except for a qualifying 90% subsidiary that itself uses the funds for a qualifying activity.

SEIS Advance Assurance Eligibility

Advance Assurance is HMRC’s non-binding view that a proposed share issue would likely qualify. It is not mandatory, but most angels expect it. HMRC usually wants your business plan, use-of-funds, company/ownership details and, in many cases, evidence of potential investors. (Undo Capital auto-fills and validates these packs.)

EIS Eligibility Criteria for UK Startups

The EIS requirements in the UK echo SEIS but allow for larger, slightly more mature companies, and they add annual/lifetime fundraising caps.

EIS Company Conditions

- Age: Typically ≤7 years since first commercial sale at the time of the first risk-finance investment; extended to ≤10 years under certain tests for knowledge-intensive companies (KICs).

- Gross assets: ≤£15m pre-money and ≤£16m post-money at the time of issue. Employees <250 (or <500 for KICs).

- Unquoted: As with SEIS, companies must be unquoted on a recognised stock exchange (AIM and AQSE Growth are not recognised markets for this test).

- Funding limits: Up to £10m in any rolling 12-month period and £24m lifetime across risk-finance schemes (EIS/SEIS/VCT/SITR). For KICs, £20m per 12 months and £40m lifetime.

EIS Qualifying Trades

What is EIS eligibility at the trade level? Under the EIS requirements in the UK, a company must carry on a commercial, profit-seeking trade and must not conduct excluded activities to a substantial extent. HMRC’s Venture Capital Schemes Manual explains that “excluded activities” include, among others: dealing in land/shares/commodities, financial services (banking, insurance, money-lending), leasing, property development, and certain energy activities. If you’re a parent company, HMRC looks at the group as a whole when assessing whether non-qualifying activities are “substantial.”

HMRC does not define “substantial” in statute; however, within its Venture Capital Schemes Manual, HMRC states it will not normally regard activities as ‘substantial’ if they amount to less than 20% of the whole business. Founders typically measure this by turnover, assets, and management time (and keep working papers that evidence the calculation). In practice, this 20% yardstick helps EIS qualifying companies show that excluded activity is ancillary rather than core.

Two pragmatic notes for EIS qualifying trades:

- Ancillary and preparatory work for a qualifying trade is fine; the problem arises where an excluded activity becomes the spine of the business. Document your activity mix, and if you’re close to the line, consider ring-fencing or deferring anything that risks tipping you over the “substantial” threshold.

- If you operate as a group, the majority of the group’s activities must be qualifying, and HMRC aggregates activities across the group when applying the “substantial” test. Map your revenue and headcount by entity and activity before you apply.

Use of Funds & Timing

Under EIS requirements, UK, money raised by an EIS share issue must be employed in a qualifying business activity and within two years, or, where you were “preparing to trade,” within two years from when you begin trading. HMRC’s guidance is explicit on both the 2-year window and what “employed” means. In short, funds are “employed” when they’re spent for the business, but HMRC also accepts earmarking with sufficient precision for a specific qualifying purpose (backed by a credible business plan) as employment of money within the period.

The public-facing EIS page reiterates this timing and adds two critical boundaries founders often miss: you must not use EIS money to buy all or part of another business, and the investment must support growth and development and pose a real risk of loss to capital. HMRC will scrutinise any arrangements that look like capital protection. Build your budget to show deployment milestones (hiring, product, GTM, R&D) that fall well within the 24-month window.

Implementation tip (how to qualify for SEIS/EIS in practice): attach a concise “Use-of-Funds & Employment” schedule to your Advance Assurance pack, dates, cost lines, and the qualifying activity each line supports. It both answers HMRC’s questions and accelerates investor diligence.

EIS Advance Assurance Eligibility

Process mirrors SEIS. Provide the same core pack; Advance Assurance reassures investors. Undo Capital’s workflow guides you through eligibility triage, document assembly, and submission.

SEIS vs EIS Eligibility: Key Differences

SEIS/EIS Investor Requirements

Investors must qualify too; relief is for individuals subscribing for new ordinary shares in a qualifying company, subject to connection, holding period, and claim rules.

- Income tax relief caps:

- Capital gains:

- SEIS reinvestment relief (CGT): 50% exemption on reinvested gains (subject to limits/conditions).

- EIS deferral relief: gains can be deferred when reinvested in qualifying EIS shares.

- Connection rules: Investors must not be connected (generally, no >30% interest or control; associates count).

- Employment rules (SEIS): Employees (and certain associates) generally cannot claim SEIS relief unless they are directors (directors can qualify).

- Hold period/claim window: Relief depends on holding the shares for at least 3 years and claiming within HMRC deadlines (up to 5 years after 31 January following the tax year of investment).

The Risk-to-Capital Condition (Both Schemes)

HMRC’s modern cornerstone: the company must intend to grow and develop over the long term, and the investor’s capital must be at significant risk. “Asset-backed” or capital-protected structures fail this test. If your model reads like a loop to return cash quickly to investors, eligibility falters. Bake growth and risk into your plan, and document both.

Common Reasons Startups Fail SEIS/EIS Eligibility

Consider this an SEIS eligibility checklist / EIS eligibility checklist in narrative form, founder-tested, HMRC-proofed:

- Sequencing errors (SEIS before EIS): If you plan to use both schemes, issue SEIS shares before any EIS shares. HMRC is explicit: “Once shares are issued under the Enterprise Investment Scheme, then the company cannot issue shares under the Seed Enterprise Investment Scheme.” In addition, you can’t raise SEIS and EIS on the same day; EIS must be at least one day after any SEIS investment. Excluded activities creeping over 20%.

- Using funds improperly: Spending outside qualifying business activity or missing the 3-year (SEIS) / 2-year (EIS) windows.

- Ignoring investor connection rules: A friendly angel with options, loans, or side agreements can accidentally trip the 30% tests of connection.

- Cap misreads: Miscounts EIS £10m/12 months and £24m lifetime across all risk-finance schemes (or £20m/£40m for KICs).

- Quoted-company traps: Listing on a recognised stock exchange (Main Market) is disqualifying; AIM and AQSE Growth are not recognised for these tests, so AIM-only companies remain unquoted for EIS/SEIS.

- Advance Assurance under-prepared: Submitting without investor interest, a clear use-of-funds schedule, or a credible growth plan that meets risk-to-capital.

How to Check Your Eligibility and Next Steps

Here’s a crisp how-to qualify for the SEIS/EIS process: one hour of disciplined prep can save three weeks of back-and-forth.

Founder’s SEIS/EIS self-check:

- Stage & size:

- SEIS: new trade ≤3 years, ≤£350k assets, <25 employees, ≤£250k total SEIS.

- EIS: generally ≤7 years since first sale (≤10 for KICs), ≤£15m assets pre-issue, <250 employees (<500 for KICs).

- Trade test: Qualifying trade; excluded activities ≤20% by reasonable measure.

- Risk-to-capital: Growth and development at risk; no capital protection.

- Use-of-funds: SEIS 3 years; EIS 2 years; mapped to hiring, product, GTM, or R&D.

- Round structure: If combining, SEIS shares first, then EIS (see note above); make sure ordinary shares are full-risk.

- Investor fit: Individual investors, not connected, intending to hold 3+ years; check their tax relief goals (SEIS 50% up to £200k; EIS 30% up to £1–2m).

- Advance Assurance: Prepare a credible dossier; include business plan, financials, cap table, draft term sheet/share rights, and investor letters.

Where Undo Capital helps: Run a fast eligibility check, ingest your plan and model, auto-fill the HMRC form, and route the pack for expert review and submission. Post-approval, the platform sequences SEIS/EIS share issues, generates SH01/board minutes, and files SEIS1/EIS1, with investor certificates tracked to completion. It’s purpose-built to keep you compliant while you close the round.

Turn SEIS/EIS Eligibility into Action with Undo Capital

The SEIS eligibility criteria and EIS eligibility criteria do more than gate tax relief: they shape how you design your round, justify the size of your raise, and prove that growth, not shelter, is the aim. If you’re asking who qualifies for SEIS/EIS, you now have the working definitions and a checklist you can run in an afternoon. Get the conditions right, and everything downstream, AA, share issue, compliance, moves cleanly.

To turn this from knowledge into motion, use Undo Capital. Start with the Eligibility Checker, build SEIS/EIS Advance Assurance with AI-assisted forms and expert review, then sequence share issues and file SEIS1/EIS1 with investor certificates tracked to the finish. Less time in paperwork; more time closing your round.

FAQs

What companies are eligible for SEIS?

Companies with a new qualifying trade up to 3 years old, ≤£350k gross assets, and <25 employees may qualify. They must be unquoted, carry on a qualifying trade, and spend funds within 3 years on growth/R&D or preparations to trade. The lifetime SEIS cap is £250k.

What companies qualify for EIS?

Generally, companies ≤7 years from first commercial sale (or ≤10 for KICs), with ≤£15m gross assets pre-issue and <250 employees (<500 for KICs). They must be unquoted, carry on a qualifying trade, and observe the £10m per 12 months / £24m lifetime funding caps (higher for KICs).

Can a company apply for both SEIS and EIS?

Yes, many seed rounds blend both. The practical rule is SEIS first, then EIS, because prior EIS/VCT funding would block SEIS. Founders commonly issue SEIS shares first, then EIS shares, to comply. Plan your allocations and dates accordingly. (Sequencing is an operational inference; HMRC explicitly bars SEIS after prior EIS/VCT).

What trades do not qualify for SEIS/EIS?

“Excluded activities” include, among others, dealing in land/commodities/shares, banking/insurance/money-lending, leasing, property development, and certain energy activities. You may do some excluded activity, but not to a substantial extent, HMRC “normally accepts” ≤20% as not substantial.

How do investors qualify for SEIS/EIS tax relief?

They must subscribe for new, full-risk ordinary shares in a qualifying company, not be connected (>30% tests/associates) and typically hold shares for ≥3 years. Relief caps: SEIS 50% up to £200k; EIS 30% up to £1m (or £2m if ≥£1m in KICs); deferral (EIS) and reinvestment relief (SEIS) apply under conditions.

References

- SEIS Before EIS — Official HMRC Sources

- HMRC Intro Note: EIS/SEIS (PDF)

- Apply to Use the Seed Enterprise Investment Scheme (SEIS)

- SEIS Expansion Policy Note

- HMRC Manual: VCM34020 — SEIS/EIS Interaction

- Apply for Advance Assurance

- Apply for the Enterprise Investment Scheme (EIS)

- Tax Relief for Investors (SEIS/EIS)

Disclosure Notice: This communication is issued by Undo Capital Limited (“Undo Capital”) and is provided strictly for informational purposes only. It contains general information and should not be relied upon as accounting, business, financial, investment, legal, tax, or other professional advice. Undo Capital is not regulated by the Financial Conduct Authority (FCA) and does not provide investment, financial, or tax advice. Our services are designed to assist startups and businesses with company formation, legal agreements, and funding-related documentation. Nothing in this communication constitutes, or should be construed as, a recommendation, offer, or solicitation to purchase or sell any security or financial instrument.

Participation in startups and early-stage enterprises involves significant risk. Such investments may be illiquid, may not generate dividends, may be subject to dilution, and may result in the total loss of invested capital. Any decisions or actions that may affect your business or personal interests should be taken only after seeking advice from suitably qualified professional advisors, and should form part of a balanced and diversified portfolio. This communication may contain links to third-party websites. The inclusion of such links does not imply endorsement, approval, investigation, or verification by Undo Capital. We accept no responsibility or liability for the content, accuracy, or use of information contained on any third-party websites.

Latest articles

%20Explained%20for%20UK%20Founders.jpg)

Share Incentive Plan (SIP) Explained for UK Founders

S431 Election Explained: What UK Founders Must Do When Issuing Shares to Employees