How To Build A Cap Table For Your Startup (Step‑By‑Step)?

- Messy ownership records scare investors. Incomplete capitalisation tables and unclear ownership percentages delay diligence and often reduce valuations. A clear capitalisation table signals professionalism and reduces funding friction.

- Dilution surprises happen. Failing to model the option pool, SAFEs or convertible notes up front leads to nasty dilution shocks during funding rounds. You need a fully diluted cap table and simple dilution analysis to stay in control.

- Legal compliance matters. In the UK, the statutory register of members is mandatory, while the startup cap table isn’t, but investors expect both to reconcile. Keeping your cap table aligned with Companies House filings and the shareholder register avoids legal headaches and investor mistrust.

If you are wondering how to build a cap table for your startup, you’re not alone. Many founders hear the term but aren’t sure what a capitalisation table is or why venture investors keep asking for it. A cap table (short for capitalisation table or capitalisation table in UK spelling) is a detailed snapshot of your company’s ownership: who owns what, what instruments they hold (shares, options, warrants or convertible notes) and what those holdings mean in terms of percentage ownership.

Building a simple, investor‑ready startup cap table is one of the first financial tasks for founders, especially if you plan to raise funding. A clean record shows you understand equity mechanics, can manage dilution analysis and that your governance aligns with UK expectations.

This procedural guide explains how to build a cap table for your startup step‑by‑step using simple tools like Google Sheets or Excel. You’ll learn the cap table meaning, see a cap table example, decide when to use a cap table template versus software, model a fully diluted cap table, and align your ownership records with your legal obligations.

Cap Table Meaning: What It Is and Why It Matters?

A cap table is the living record of your company’s ownership and the rights attached to that ownership. It lists shareholders, the number of shares held, share classes (ordinary/common or preference/preferred), the price paid, and any convertible instruments or employee stock options. Cap tables can also show the difference between issued shares and the fully diluted cap table, which adds in ungranted options and convertible notes as if they converted. Unlike a simple list of shareholders, a cap table models how ownership shifts over time as you raise money, create an option pool, or issue convertible notes/SAFEs.

Why do investors care? A clean cap table makes due diligence smooth. It reveals whether founders have retained a meaningful stake, whether early advisers hold too much dead equity, and whether there is space for future hires and fundraising. Without accurate ownership information, investors cannot assess dilution risk. Moreover, UK founders must keep a statutory shareholder register that serves as the legal record of ownership, and it must be kept up to date and available for inspection. While the cap table is not legally required, it should reconcile with the register. Getting both right builds trust with angels, venture funds, accountants and lawyers.

Cap Table vs Cap Structure

Founders often confuse the terms cap table and cap structure. Your cap table is a table, typically a spreadsheet or software interface, that records issued shares and ownership. Your cap structure is the broader mix of equity and debt instruments: ordinary shares, preference shares, convertible notes, SAFEs and warrants. Understanding cap structure helps you model how new funding instruments change ownership and rights. The cap table is your working tool to track that structure and anticipate changes during fundraising. When investors ask for a fully diluted cap table, they’re asking to see the cap structure as if every instrument converted.

What Does a Cap Table Include?

A robust capitalisation table includes several data points:

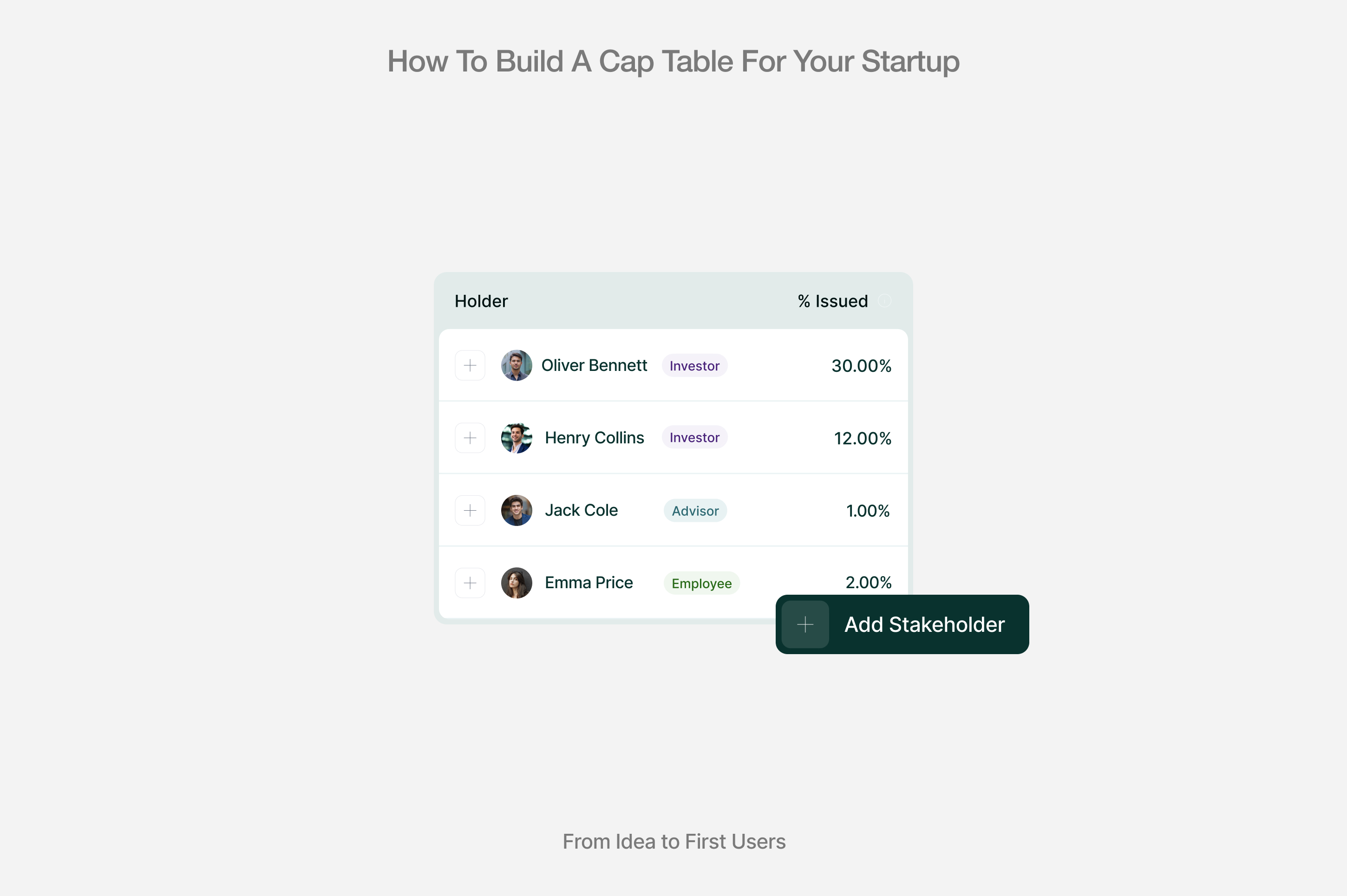

- Shareholder list and security type. Each line identifies the stakeholder (founders, employees, angel investors, venture funds) and the instrument they hold (ordinary shares, preference shares, options, warrants, convertibles). This is the bedrock of cap table management.

- Number of shares and share classes. For every stakeholder, record the number of shares issued and the share class (e.g., Ordinary A, Preference B). Share classes matter because they confer different rights, such as liquidation preference or anti‑dilution protections.

- Price paid and investment date. Cap tables track at what price and when shares were issued. These figures anchor pre‑money and post‑money valuations in future rounds.

- Ownership percentage (issued and fully diluted). Two views are essential: the issued cap table shows ownership based on currently issued shares; the fully diluted cap table assumes all options are exercised, and all convertibles convert, giving investors a clearer picture of potential dilution.

- Vesting schedule and status. For founders and employees with unvested shares, record the vesting start date, cliff, and end date. A typical founder vesting schedule in the UK is four years with a one‑year cliff.

- Convertible instruments. SAFEs, convertible notes or ASAs should be logged separately, including principal invested, conversion cap or discount, and conversion trigger.

- Notes on rights and terms. Capture important rights: liquidation preference, anti‑dilution protection, and any board seats. A short note in the cap table helps you remember which investors have special rights and ensures nothing is missed when drafting agreements.

Some advanced cap tables also include a mini waterfall analysis that projects payout splits under various exit scenarios. This level of detail is not necessary for an early-stage startup cap table, but understanding liquidation preference and exit outcomes can become important when raising Series A or beyond.

Issued vs Fully Diluted

In this simple cap table example, Founders A and B have issued shares totalling 900,000, while the investor owns 100,000 preference shares. A reserve of 200,000 options is authorised but ungranted. On an issued basis, Founder A owns 60%; on a fully diluted basis, after accounting for the option pool, Founder A owns 48%. This illustrates why you need to model the fully diluted cap table early to understand the impact of an option pool and avoid surprises.

Step 1 – Decide Your “Minimum Viable Cap Table” Approach

Before you start plugging numbers into Google Sheets or Excel, decide what level of detail you need today. A simple cap table should suit a small pre‑seed team. It contains founders’ shares, any early angels, and a placeholder option pool. Using a spreadsheet or a downloadable cap table template from reputable sources keeps things transparent and low‑cost. You can build the template yourself: use one tab for summary and separate ledger tabs for each share class or security type.

When does a spreadsheet become risky? Once you have multiple share classes, a large option pool, secondary transactions, convertible notes/SAFE instruments, or different vesting schedules, formulas get messy. Version control becomes a nightmare when you share the file with lawyers, accountants and investors. At that point, switching to dedicated cap table management software makes sense. Good software tracks every equity event, generates board resolutions, and keeps your statutory register aligned with Companies House filings.

Cap Table Template vs Cap Table Software

Many founders start with a cap table template because it’s free and flexible. Templates suit early-stage companies with simple ownership structures and few stakeholders. However, they lack error‑checking, can’t simulate dilution, and risk being outdated when multiple people edit them. Cap table management software, such as the modern tool offered by Undo Capital, automates calculations, stores documents securely, allows for scenario modelling and ties directly into SEIS/EIS documentation and share issuance workflows. The trade‑off is cost, but the investment often pays off when you prevent errors or lost investor confidence.

Step 2 – Gather the Inputs Before You Build

Building a cap table is easier when you collect all the relevant documents and data in advance. Here’s a checklist:

- Total authorised shares. Know how many shares your articles allow you to issue (or the UK equivalent). In early UK companies, you typically authorise a large number (e.g., 10 million) to provide flexibility. If you haven’t thought about this, talk to your company secretary or legal advisor.

- Founders and share splits. Record how many shares each founder holds, the vesting schedule, and any cliff or reverse vesting terms.

- Existing investors. Note their names, the amount they invested, the price per share, the share class, and the date of investment. This sets your pre‑money cap table for new rounds.

- Option pool plan. Decide on the size of your option pool and whether it will be created pre‑money or post‑money. Seed rounds in the UK usually target an option pool between 10–15% fully diluted. Clarify the number of options granted vs ungranted.

- Convertible notes/SAFEs/ASAs. Document each instrument: principal invested, interest rate (if any), valuation cap, discount rate and conversion events. Add expected conversion shares once they convert.

- Share classes and rights. Collect any term sheets, subscription agreements or shareholder agreements that specify rights like liquidation preference or anti‑dilution clauses.

- Legal registers. Pull your latest register of members from your company secretary or records. Since 18 November 2025, UK companies must hold a register of members at their registered office and include all shareholders and share classes in the annual confirmation statement. Make sure your cap table will reconcile to this statutory record.

Step 3 – Build the Spreadsheet Structure

Once you have your inputs, set up your cap table structure. At a minimum, your main tab should include these columns:

- Stakeholder. Name of the shareholder or beneficiary (founder, employee, investor).

- Security type. Ordinary shares, preference shares, options, warrants, convertible notes, ASA/SAFE.

- Class/series. If you have multiple share classes or series (e.g., Series A preference), record which class each issuance belongs to.

- Number of shares/units. For shares, list the number issued; for options, track granted versus ungranted; for convertibles, record principal or expected shares.

- Price paid. Amount per share paid by the stakeholder. For options, record the exercise price.

- Investment or grant date. The date shares were issued or options granted. Dates are important for vesting and tax purposes.

- Vesting status. If the shares or options are subject to vesting, indicate vested/unvested status and include key dates.

- Ownership %. Calculate both issued ownership and fully diluted ownership automatically using formulas.

- Notes/rights. Use a notes column to flag special rights, such as liquidation preference, board seats or SEIS/EIS eligibility.

Common Formats Investors Expect to See

Investors are accustomed to certain formats. A well‑structured cap table will have a summary tab that provides the big picture: total shares outstanding, total options granted, fully diluted share count and ownership percentages. The summary tab should also break down ownership by founders, employees (granted and ungranted options), investors and others. Supporting tabs or ledger sheets detail each equity event (founder issuances, option grants, convertible note conversions, etc.). Including both high‑level and granular views makes it easier for investors to navigate your cap structure.

Step 4 – Enter Founder Equity Correctly

Founders should allocate shares thoughtfully. Give yourselves enough equity to be motivated long‑term while leaving room for the team and future investors. Many early founders issue 100% of their shares on day one, only to realise later that investors expect vesting. A popular choice in the UK is a four‑year vesting schedule with a one‑year cliff, meaning no shares vest until the one‑year mark, after which they vest monthly or quarterly. Some agreements start with 0% vested at grant and accelerate if the founder stays on board; this protects the company from dead equity, shares held by people no longer contributing.

When adding founder equity into your cap table:

- Record the number of shares each founder holds and the date of issuance.

- Note the vesting schedule: start date, cliff and end date. A typical schedule is “four years, one‑year cliff.”

- Include any good leaver and bad leaver provisions. If a founder departs early (bad leaver), unvested shares may be repurchased for nominal value and reallocated.

- Don’t forget tax considerations; talk to an accountant about tax elections and whether you qualify for EMI or CSOP plans for options.

A clear record of founder equity will reassure investors that the founding team is aligned and that there is room in the cap table for employees and funding rounds.

Step 5 – Add an Option Pool and Show Dilution Clearly

An option pool reserves shares for future employee stock options, advisors or consultants. Investors expect this pool to exist before they invest. There’s a strategic decision to make: create the pool pre‑money (so it dilutes existing shareholders) or post‑money (so dilution is shared among new investors). A pre‑money pool increases investor ownership because the pool dilutes founders before investors buy in; a post‑money pool distributes dilution across all shareholders.

When building your cap table:

- Decide the pool size based on your hiring plan. If you plan to grant 5% to early employees and 5% for future hires before the next round, a 10% pool is reasonable. Large pools (25%) may signal poor planning or over‑incentivisation.

- Create separate rows for the option pool reserved (ungranted) and for granted options. Granted options should show the individual option holder, the number of options, vesting schedule, exercise price and grant date. Ungranted options appear in the fully diluted calculation but do not belong to any specific person.

- Show both issued and fully diluted ownership. For example, if your company has 1 million issued shares and you authorise a 200,000‑share option pool (of which 100,000 are granted), the fully diluted share count becomes 1.2 million. Each stakeholder’s fully diluted percentage equals their shares divided by 1.2 million.

Do Option Holders Appear on a Cap Table?

Option holders appear once their options are exercised or vested, depending on how you track them. Some cap tables list granted options as separate rows even before exercise to show who has been promised equity. Others list only issued shares and treat options as a single line. Be transparent about your method and use the notes column to clarify. Investors care about how many options are outstanding and how much additional dilution may come from future grants. A fully diluted cap table should always include ungranted options as if they were issued.

Step 6 – Add Investor Equity and Share Classes

When you raise money, you issue new shares to investors. Most UK seed rounds involve preference shares, which confer additional rights relative to ordinary shares. For example, preference/preferred shares typically come with a liquidation preference, meaning investors get their investment back (often 1× the amount invested) before ordinary shareholders receive proceeds. They may also include anti‑dilution protection and sometimes voting rights. Ordinary shares (also called common shares) are the base class issued to founders and employees; they rank behind preference shares for dividends and liquidation.

When adding investors to your cap table:

- Record the pre‑money cap table: total issued shares and their distribution before the round. Determine the price per share based on your pre‑money valuation and the number of issued shares.

- Calculate how many new shares you’ll issue. For example, if your company has a pre‑money valuation of £5.6 million and you raise £2 million, the post‑money valuation is £7.6 million. If there are 1 million shares outstanding before the round, the pre‑money price per share is £5.60. A £2 million investment at £5.60 per share yields 357,143 new shares. The investor owns £2 million ÷ £7.6 million = 26.3% of the post‑money company (simplified example).

- Add a row for each investor with their share count, class and price paid. Note any special rights, such as liquidation preference.

- Recalculate ownership percentages across all stakeholders on both the issued and fully diluted basis.

Worked Dilution Example (Founders → Option Pool → Seed Round)

Let’s walk through a simple dilution scenario. Imagine two founders, Alice and Bob, each holding 500,000 ordinary shares (1 million total). They create a 15% option pool (176,470 shares on a fully diluted basis) and raise a £1.5 million seed round at a £6 million pre‑money valuation. We use the equation:

- Pre‑money price per share: £6 million ÷ 1,000,000 = £6 per share.

- Fully diluted shares before round: 1,000,000 / (1 − 15%) = 1,176,470 shares.

- New shares for investors: Investment ÷ price per share = £1.5 million ÷ £6 = 250,000 shares.

- Post‑money shares: 1,176,470 + 250,000 = 1,426,470 shares.

- Ownership after round:

- Alice: 500,000 ÷ 1,426,470 ≈ 35.1%

- Bob: 500,000 ÷ 1,426,470 ≈ 35.1%

- Option pool (ungranted): 176,470 ÷ 1,426,470 ≈ 12.4%

- Investor: 250,000 ÷ 1,426,470 ≈ 17.5%

This example shows that the option pool reduces founder ownership even before the round, and the new investors further dilute both founders and the option pool. Modelling these numbers up front allows you to negotiate pool size and pre‑money valuation intelligently.

Step 7 – Model Convertibles (SAFEs/Notes) without Breaking Your Cap Table

Early‑stage UK companies often raise capital via convertible notes (CLNs), SAFEs or Advance Subscription Agreements (ASAs). These instruments are agreements to issue shares later, usually triggered by a priced round. Each has unique features:

- Convertible loan notes (CLNs) are debt instruments that accrue interest and convert into shares at maturity or at the next funding round. They may have a valuation cap (maximum valuation at conversion) or a discount (percentage discount to the next round price).

- Advance Subscription Agreements (ASAs) are equity instruments under UK law. They don’t accrue interest or have a maturity date. For SEIS/EIS eligibility, ASAs must be straightforward equity and convert within six months of payment.

- Simple Agreements for Future Equity (SAFEs) are similar to ASAs but originally developed in the US. They are equity instruments that convert upon a priced round using a discount or cap; they often lack maturity or interest provisions.

To model convertibles in your cap table:

- Create a separate section for each instrument. Record the principal, discount rate, valuation cap, and date issued.

- During the convertible period (before conversion), do not include these instruments in your issued share count. Instead, estimate how many shares they would convert into at different valuations and include those figures in your fully diluted cap table.

- When you close a priced round and the convertibles convert, add the new shares to your issued share count. Remove the convertible from the outstanding instrument list.

- If the instrument qualifies for SEIS/EIS, ensure the cap table shows the correct share type (ordinary shares) and that conversion happens within the required timeframe.

Modelling convertibles separately helps prevent “phantom dilution,” where founders and investors underestimate the impact of notes on final ownership. Modern cap table software can automatically convert these instruments based on your chosen discount or valuation cap, which reduces errors and speeds up fundraising.

Step 8 – Run Accuracy Checks that Investors Will Ask For

Before sharing your cap table with investors or including it in a data room for due diligence, run these checks:

- Totals match. Ensure the number of issued shares plus ungranted options equals the authorised shares if you are close to your limit. Check that your fully diluted share count matches the sum of all ownership percentages.

- Ownership percentages sum to 100%. Both the issued and fully diluted columns must add up to 100%. If not, formulas may be missing ungranted options or convertibles.

- Round‑to‑round continuity. Verify that share counts carry over correctly from one funding round to the next. Many spreadsheet errors stem from copying tabs without updating formulas.

- Rights recorded. Make sure any special rights, like liquidation preference or anti‑dilution provisions, are annotated. Investors need to know if preference shares have 1× or 2× liquidation preference or if they are participating.

- Register reconciliation. Cross‑check the cap table against your statutory shareholder register. From 18 November 2025, UK companies no longer need to keep registers of directors, secretaries or PSCs, but they must maintain an up‑to‑date register of members at the registered office. The cap table should reconcile with the register and your confirmation statement filed at Companies House.

Step 9 – Keep Your Cap Table Investor‑Ready Over Time

A cap table is not a static document. Each time you issue new shares, grant options, allow options to vest, issue or convert a SAFE/ASA, or close a secondary sale, you must update your cap table. Best practice is to update it immediately after any equity event and, at a minimum, before sending updates to investors or filing your confirmation statement. Use role‑based access control to let advisors and investors view the latest version without editing rights. If you rely on spreadsheets, implement strict version control (e.g., using a locked master sheet). If you upgrade to software, ensure that it integrates with share issuance workflows and due diligence preparation.

UK Hygiene: Cap Table vs Shareholder Register

In the UK, the cap table is not legally mandated. The register of members (shareholder register) is the legal record of ownership and must be kept at your registered office or an alternative inspection location. The register lists shareholder names, addresses, class of shares and holdings. From 18 November 2025, there is no requirement to keep separate registers of directors or PSCs, but the register of members remains mandatory. Your cap table should mirror this register for issued shares. Where they differ, typically because the cap table models unissued options or future conversions, make sure the differences are clearly labelled. Reconciling your cap table and register avoids confusion during due diligence and ensures you file accurate confirmation statements with Companies House.

Common Mistakes When Building a Startup Cap Table

Even experienced founders stumble when managing equity. Here are some pitfalls to avoid:

- Mixing issued vs fully diluted numbers. Listing ungranted options as issued shares artificially inflates share counts and misleads investors. Keep separate columns for issued and fully diluted ownership and label them clearly.

- Forgetting ungranted options. It’s easy to track only granted options, but investors want to see the full impact of your reserved option pool. Always include unallocated options in your fully diluted cap table.

- Not tracking convertibles early. Ignoring SAFEs, ASAs or CLNs until they convert results in unexpected dilution. Log them when they are signed and estimate conversion shares so you’re not surprised later.

- Spreadsheet errors and version drift. Copy‑pasting formulas can lead to mistakes. Without a single source of truth, multiple versions create confusion and erode investor confidence. Use checksums or adopt the cap table software.

- Misaligned statutory records. Failure to reconcile your cap table with the register of members and Companies House filings can lead to legal issues. The register is the authoritative record, so keep it aligned.

Cap Table Template and Tools

The easiest way to start is with a free or low‑cost cap table template. Build one yourself or download a version that includes summary and ledger tabs. Include formulas to calculate ownership percentages and fully diluted counts. Add macros or pivot tables to generate charts if you’re comfortable. However, the complexity of your cap structure will likely outgrow a template. When you begin to issue multiple share classes, manage frequent option grants, process secondary transactions, or prepare for due diligence, spreadsheets become brittle. Mistakes in formulas or hidden cells can lead to costly errors.

Dedicated cap table management software solves these issues. It automates calculations, provides a clear audit trail, and connects directly to other workflows, such as SEIS/EIS applications, share issuance (SH01), investor relations and reporting. Modern platforms let you visualise ownership, model dilution scenarios, run waterfall analysis, and share role‑based access with investors and advisors. They also integrate with Companies House filings, ensure GDPR‑compliant data handling and maintain a clear history of changes. Using software early reduces headaches later and signals to investors that you take governance seriously.

How Does Undo Capital Help?

Undo Capital offers a modern cap table management tool tailored to UK founders.

- SEIS/EIS automation. Undo Capital auto‑fills HMRC Advance Assurance applications using your deck and financials, files SEIS1/EIS1 compliance statements, and tracks SEIS/EIS relief for each investor.

- Share issue & compliance. Generate SH01 forms, board minutes and share certificates automatically and file them with Companies House, ensuring that your cap table aligns with your statutory register.

- Data room & investor portal. Securely share documents, financials and updates with investors through a built‑in data room, track investor interest and soft commitments, and support due diligence preparation.

- Option pool and EMI schemes. Set up and manage option pools, calculate EMI valuations, and maintain vesting schedules, reducing administrative overhead.

- Integrated contracts. Access templates for founder agreements, shareholder agreements, convertible loan notes (CLNs) and Advance Subscription Agreements (ASAs), ensuring consistent documentation throughout your fundraising process.

- Board & shareholder management. Coordinate board resolutions, manage secondary share sales, and produce investor reports from a single interface.

Because Undo Capital aligns with HMRC and Companies House processes, everything you do inside the platform is built to be audit‑ready and regulation‑safe. By using Undo Capital, founders avoid messy spreadsheets, reduce risk in funding rounds, and keep investors informed.

FAQs

What is a cap table used for?

A cap table (or capitalisation table) records who owns what in a company and serves as the roadmap for equity decisions. Investors use it to verify founders’ stakes, assess dilution risk, and ensure that employees have enough option pool allocation. Founders use it to model funding rounds, negotiate valuations and prepare for due diligence. It also helps reconcile the shareholder register, ensuring legal compliance.

What should a startup cap table include?

A startup cap table should list every stakeholder, security type, share class, number of shares, price paid, date issued, vesting status and ownership percentage. Include convertible instruments (e.g., SAFEs, ASAs, convertible notes), ungranted options and any special rights. Provide both issued and fully diluted cap table views. Record notes about rights such as liquidation preference, vesting schedule, or SEIS/EIS status to facilitate due diligence.

What is a fully diluted cap table?

A fully diluted cap table shows ownership as if all outstanding instruments convert into ordinary shares. It accounts for ungranted options, unvested options and convertible notes/SAFEs at their conversion cap or discount. The fully diluted view helps founders and investors understand maximum potential dilution and informs discussions on valuation and option pool size.

Do option holders appear in a cap table?

Option holders usually appear once options are granted, even before they are exercised. You can list them in a separate section with the number of options, vesting schedule and exercise price. For ungranted options, show the total reserved pool in the fully diluted calculation. Investors care about the total pool and who has been promised equity.

Do convertible notes/SAFEs go on a cap table?

Yes. You should log convertible notes, SAFEs and ASAs when they are issued, including the principal, discount or valuation cap, and conversion trigger. Until conversion, they don’t appear in the issued share count but must be reflected in the fully diluted cap table. Convertibles can significantly affect future ownership, so modelling them early prevents surprises.

References

Disclosure Notice: This communication is issued by Undo Capital Limited (“Undo Capital”) and is provided strictly for informational purposes only. It contains general information and should not be relied upon as accounting, business, financial, investment, legal, tax, or other professional advice. Undo Capital is not regulated by the Financial Conduct Authority (FCA) and does not provide investment, financial, or tax advice. Our services are designed to assist startups and businesses with company formation, legal agreements, and funding-related documentation. Nothing in this communication constitutes, or should be construed as, a recommendation, offer, or solicitation to purchase or sell any security or financial instrument.

Participation in startups and early-stage enterprises involves significant risk. Such investments may be illiquid, may not generate dividends, may be subject to dilution, and may result in the total loss of invested capital. Any decisions or actions that may affect your business or personal interests should be taken only after seeking advice from suitably qualified professional advisors, and should form part of a balanced and diversified portfolio. This communication may contain links to third-party websites. The inclusion of such links does not imply endorsement, approval, investigation, or verification by Undo Capital. We accept no responsibility or liability for the content, accuracy, or use of information contained on any third-party websites.

Latest articles

Share Certificate UK: What It Is, What It Must Show, and How to Issue One

UK Trademark Registration for Startups: Step‑by‑Step Guide