Share Classes Explained: What UK Startups Must Know Before Fundraising

- Compliance determines eligibility. SEIS/EIS relief hinges on ordinary shares only, no special dividends, no redemption and no liquidation preference. Mislabelling alphabet shares or founder stock can turn them into non‑compliant shares and jeopardise tax relief.

- Preferences appear later. Preference shares with liquidation preference and priority dividends are common from Series A onward, but will disqualify early‑stage SEIS/EIS rounds. Pre‑seed and seed founders should keep their cap table clean with one class of ordinary shares.

- Docs must align. Articles of Association, shareholder agreements and SH01 filings must describe voting rights, dividends and redemption consistently. Ambiguities create “hidden” preferences that HMRC can deem disqualifying.

Raising capital in the UK is not simple. Every founder competes for attention while dealing with strict regulations and cautious investors. Yet one overlooked choice, which shares the same issues UK startups face, can decide whether a round closes or collapses.

Many early-stage teams treat share class decisions as paperwork. They assume any structure will do. It will not. Under SEIS share class rules, a single preference right or redemption clause can wipe out eligibility and force investors to walk away.

This article explains how ordinary shares UK work, why preference shares UK trigger risk, and how share classes UK startups can structure a clean cap table without breaching SEIS/EIS. You will learn which rights are permitted, which are prohibited, and how to design a UK fundraising share structure that protects SEIS relief and investor confidence from the start.

Why Getting Share Classes Right Matters?

The UK government encourages investment in early‑stage businesses through the Seed Enterprise Investment Scheme (SEIS) and Enterprise Investment Scheme (EIS). To qualify, startups must issue only ordinary shares that are fully at risk; they cannot promise fixed dividends, guaranteed returns or preferential payouts on a sale.

Stray outside these share class restrictions in the UK, and your investors lose their tax relief. Meanwhile, venture capital rounds later in the journey may introduce preference shares with liquidation rights, anti‑dilution provisions and super‑voting powers. Choosing the wrong structure too early can complicate your cap table, deter future investors and trigger an HMRC inquiry.

Undo Capital’s platform simplifies this complexity by automating share issuance and cap table modelling. Its workflows mirror HMRC processes and Companies House record structures, ensuring every submission and share issue is compliant and audit‑ready. With the right knowledge and tools, founders can design a share structure that supports both tax‑efficient fundraising and long‑term growth.

What Are Share Classes? The UK Legal Definition

A share class groups together shares that carry the same rights. UK companies can issue multiple classes, each with tailored voting, dividend and capital rights, as long as these rights are clearly stated in the Articles of Association, share classes and any shareholder agreements. HMRC’s Capital Gains Manual explains that companies may issue voting and non‑voting ordinary shares, preference shares and deferred shares; the difference between classes is expressed through three principal rights: priority dividends, voting restrictions and preferential rights on liquidation.

Why Share Classes Exist?

Share classes allow founders to fine‑tune control and incentives:

- Distribution of economic rights. Different dividends and exit priorities enable founders to reward early backers or family members without relinquishing voting control. For instance, alphabet shares can carry varied dividend rates while retaining equal capital rights.

- Protection of investors. Preference shares give investors priority on dividends and capital in a winding‑up. HMRC notes that preference shares typically provide fixed dividends, restricted voting rights and preferential rights to a distribution on winding up.

- Retaining control. Non‑voting shares and super‑voting founder shares allow companies to raise funds without diluting decision‑making power. Founder shares may include enhanced voting rights to preserve influence through later funding rounds.

Core Rights that Define a Share Class

Designing share classes involves adjusting several key rights within the Articles:

- Voting rights. Ordinary shares usually carry one vote per share. Startups can create non‑voting shares in the UK or enhanced voting shares for founders and investors. The Companies Act 2006 requires that any variation of voting rights be properly documented in the Articles.

- Dividend rights. Shares can have variable dividend rates or priority dividends. HMRC warns that cumulative or variable dividends count as preferential rights and will disqualify SEIS/EIS shares.

- Capital/exit rights. Preferences determine who gets paid first when a company is sold or wound up. Preference shares may entitle holders to priority distributions on liquidation.

- Conversion and redemption. Shares can be convertible into another class or redeemable for cash. Redemption and conversion terms must be explicit; redeeming or converting rights often fall outside the scope of SEIS/EIS eligibility.

- Transfer restrictions. Pre‑emption rights prevent unwanted transfers, while leaver provisions govern what happens when shareholders leave. These rules, often codified in shareholders’ agreements, protect the company and existing investors.

Establishing clear rights avoids disputes and ensures your cap table matches your investors’ expectations.

Ordinary Shares in the UK (The Standard for Startups)

Ordinary shares sit at the core of most UK fundraising share structures because they offer simple, equal rights that investors and HMRC can trust.

What Are Ordinary Shares?

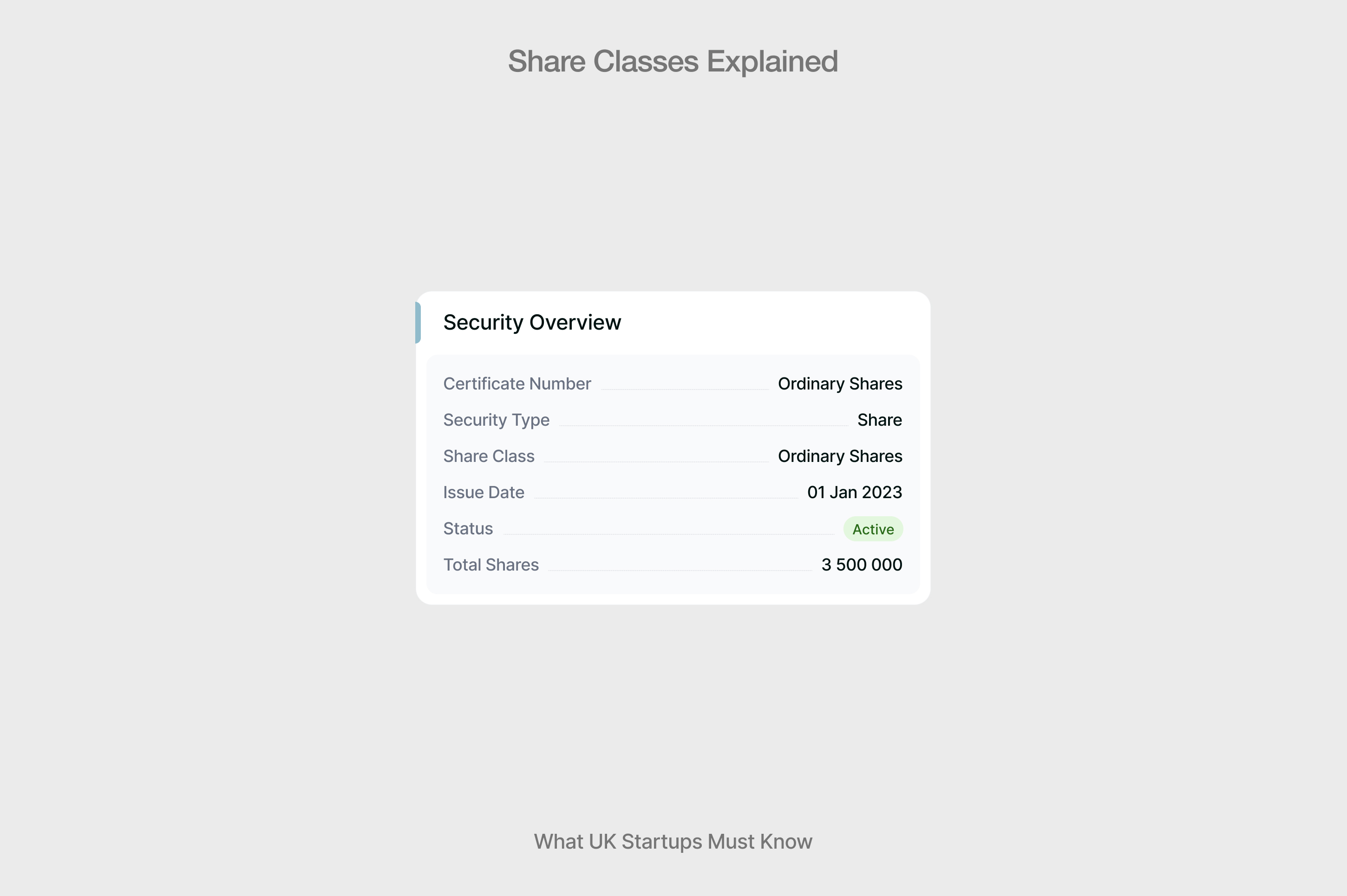

Ordinary shares in the UK are the default and most common type of equity issued by startups. Inform Direct describes them as shares that carry one vote per share, equal rights to dividends and equal rights to capital on winding up. Each shareholder’s entitlement is proportional to their ownership. Ordinary shares form the basis of an investor‑friendly UK investment share structure because they are simple, transparent and free of hidden preferences.

Why Are Ordinary Shares Required for SEIS/EIS?

HMRC’s Venture Capital Schemes Manual states that, for SEIS and EIS, the shares must be ordinary shares carrying no present or future preferential right to dividends, no preferential rights to assets on winding up, and no right to be redeemed. SEIS shares must be full‑risk ordinary shares, not redeemable and without special rights to assets; limited preferential dividends may be allowed, but cannot accumulate or be varied. In other words, only ordinary shares only SEIS/EIS qualify for tax relief; any preference, redemption, or guaranteed return creates SEIS non‑compliant shares.

What Ordinary Shares Typically Include?

- Equal voting rights. One vote per share on all matters, from appointing directors to approving transactions.

- Equal economic rights. Dividends (when declared) are distributed pro rata to the number of shares held.

- Equal liquidation rights. On a sale or winding up, ordinary shareholders share any remaining funds after creditors have been paid.

Maintaining a single ordinary class reduces complexity and keeps your cap table attractive to angel investors and crowdfunding platforms. For guidance on tracking your ownership accurately, see our cap table management guide.

Preference Shares Explained (UK Startup Context)

Preference shares create unequal rights by design, offering certain investors priority treatment that can reshape payouts and control in a funding round.

What Are Preference Shares?

Preference shares UK (also called preferred shares) give holders priority over ordinary shareholders for dividends or return of capital. HMRC notes that a typical preference share carries preferential rights to a fixed dividend, restricted voting rights and priority over ordinary shareholders in a solvent winding up. Inform Direct explains that a 5% preference share priced at £1 pays an annual dividend of 5p, and preference shareholders are entitled to arrears of dividends and their capital ahead of ordinary shareholders.

Preference shares can be cumulative (missed dividends accrue), non‑cumulative, participating (sharing additional profits) or non‑participating. Venture capital and private equity investors often negotiate rights such as 1× or 2× liquidation preference, anti‑dilution clauses and redemption rights to protect their downside.

Why Preference Shares Are Usually Not Allowed for SEIS/EIS?

Because SEIS/EIS schemes are designed to encourage high‑risk investment, any arrangement that protects investors’ capital or guarantees returns is disqualified. HMRC’s manual explicitly states that SEIS/EIS shares must carry no preferential rights to dividends (other than non‑cumulative dividends) and no preferential rights to the company’s assets on winding up.

Preference shares with fixed dividends or liquidation preferences therefore breach the SEIS share class rules. As a result, early‑stage rounds seeking SEIS/EIS investors must issue only ordinary shares.

When Preference Shares Appear (Series A and Later)?

In later funding rounds, typically Series A or later, venture capitalists often invest through preference shares to secure downside protection. A standard VC term sheet might grant a 1× liquidation preference, meaning investors recoup their investment before ordinary shareholders in a sale.

Such terms are common in growth rounds but should be layered carefully. Overly complex preference stacks can create an “overhang” that reduces ordinary shareholders’ return in various exit scenarios. Modelling preferences using cap table modelling tools helps founders and investors understand dilution and exit outcomes.

Alphabet Shares (A, B, C Shares): Flexibility for Founders

Alphabet shares allow founders to tailor rights across different classes, adding flexibility without changing the underlying ownership split.

What Are Alphabet Shares?

Alphabet shares are ordinary shares divided into multiple classes (A, B, C, etc.) to provide flexible rights. Alphabet shares enable companies to assign different dividend rates, voting rights and capital entitlements to each class. For example, A shares may carry full voting, dividend and capital rights; B shares may lack voting rights but still receive dividends; C shares could forgo dividends in favour of enhanced capital rights.

When Are Alphabet Shares Useful?

Alphabet shares are popular in family‑owned businesses and startups that need to:

- Pay different dividends to different groups – e.g. founders versus investors, without changing ownership percentages.

- Distinguish between co‑founders’ remuneration or allocate separate classes for employee incentives.

- Offer non‑voting or restricted‑voting shares to investors who provide capital but do not need governance input.

However, companies must ensure their Articles clearly set out the rights of each class. Simply renaming shares without defining distinct rights does not create a separate class and can cause disputes later.

SEIS/EIS Compatibility Concerns

Alphabet shares are not inherently disallowed under SEIS/EIS, but they must still be ordinary shares for tax purposes. HMRC’s guidance tolerates different voting or dividend rights only if they do not confer preferences. For SEIS/EIS, alphabet shares should avoid fixed or cumulative dividends, liquidation preferences and redemption rights. In practice, many startups avoid alphabet shares in pre‑seed rounds to keep their UK investment share structure simple.

Non‑Voting Shares: Pros, Cons and SEIS/EIS Issues

Non-voting shares let founders raise money without giving up control, but the trade-off between flexibility and investor confidence can be significant.

Why Startups Issue Non-Voting Shares?

Non‑voting shares provide economic rights without voting power. Non-voting shareholders cannot vote on company matters or attend general meetings, but they often receive the same dividends as voting shareholders. Startups might issue non‑voting shares to family members, employees or passive investors to raise capital without diluting control.

Risks for Early‑Stage Investors

While non‑voting shares can protect founders’ control, they may deter sophisticated investors who demand board seats or veto rights. Non‑voting shareholders still enjoy statutory protections and can challenge unfair prejudice, so their existence does not eliminate legal risk. Additionally, issuing non‑voting shares too early can complicate later rounds if investors seek to convert them into voting shares.

SEIS/EIS Restrictions

HMRC does not explicitly ban non‑voting shares for SEIS/EIS. However, to qualify as ordinary shares, they must carry no preferential economic rights. The rights to dividends and capital must mirror those of voting shares. Any enhancement, such as priority dividends or guaranteed returns, turns them into SEIS non‑compliant shares.

Growth Shares, Flowering Shares and Other Advanced Structures

Growth shares introduce conditional rights that reward future value creation, making them powerful for incentives but risky for early-stage tax relief.

What Are Growth Shares?

Growth shares (sometimes called flowering shares or hurdle shares) enable holders to benefit only from future appreciation. Growth share carries value only if the company exceeds a specified valuation hurdle. A sale above the hurdle triggers participation, while a sale below the hurdle yields nothing. These shares are popular in mature companies that have outgrown tax‑advantaged schemes like EMI and CSOP.

When Are They Used?

Growth shares incentivise key hires, advisors or late‑joining founders. Because the shares start with minimal value, recipients pay little or no income tax upfront. They share in the upside beyond the hurdle, aligning incentives with long‑term growth. A typical plan might set a hurdle above the current share price, enabling employees to purchase shares at a nominal price.

SEIS/EIS Compliance Considerations

Growth shares are not part of the ordinary share capital; they are a separate class with conditional economic rights. Because they entitle holders only to value above the hurdle, they constitute a form of preference or option and are generally SEIS non‑compliant shares. Startups should therefore avoid growth shares until after SEIS/EIS periods have ended. Complex schemes can also trigger HMRC’s risk‑to‑capital condition if they reduce investors’ exposure to genuine risk.

Deferred Shares and Founder Shares

Deferred shares and founder shares shape long-term ownership and control, rewarding commitment but demanding careful structuring to avoid breaching SEIS/EIS rules.

Deferred Shares UK

Deferred shares are long‑term instruments issued to founders, directors or investors. Deferred shares represent a long‑term investment locked away until a major liquidity event, such as dissolution or acquisition. They may have conditions tied to performance or time (vesting), and dividends are paid only after ordinary shareholders receive a threshold. Deferred shares incentivise commitment and can grow significantly if the company performs well.

Founder Shares UK

Founder shares (also called founder stock) are issued to the founding members at or shortly after incorporation. Founder shares are a type of common stock that establishes the initial ownership among co‑founders. Key characteristics include:

- Low nominal price. Founder shares are usually issued at a very low price because the company’s fair market value at inception is minimal.

- Extra rights. Founders control the company and appoint directors; their shares may include super‑voting rights to maintain control through future rounds.

- Vesting schedules. Shares typically vest over four years with a one‑year cliff, ensuring founders remain committed.

SEIS/EIS Restrictions

In the UK, founder shares must be issued before investors subscribe for SEIS/EIS shares. These shares can still be ordinary shares so long as they carry no preferential rights. Super‑voting rights and vesting schedules are acceptable if economic rights mirror those of other ordinary shares. However, the founder shares that including liquidation preferences, fixed dividends or redemption rights would breach SEIS share class rules.

SEIS/EIS Share Class Requirements: What Founders Must Know

For early‑stage fundraising, understanding the SEIS share class rules is critical. Both SEIS and EIS require that shares issued to investors meet these conditions:

- Ordinary shares only. The shares must be part of the company’s ordinary share capital, meaning they cannot carry fixed dividends or guaranteed returns.

- No preferential rights. The shares cannot have any present or future preferential right to dividends, assets on winding up or redemption. Cumulative dividends and variable dividend rates that can be decided by the company or shareholders count as preferential rights.

- No redemption or convertible rights. Shares cannot be redeemable or convertible into a different class during the three‑year holding period.

- Cash subscription. Investors must pay for the shares wholly in cash at the time of issue.

- Full risk capital. There must be no arrangements that protect the investor’s capital or offer downside protection. HMRC’s risk‑to‑capital condition requires that investors risk more capital than they are likely to gain.

Failure to meet these conditions results in HMRC rejecting your SEIS/EIS compliance statement, causing investors to lose their tax relief. For an in‑depth checklist, see our SEIS/EIS eligibility criteria.

How Share Classes Impact Your Cap Table and Fundraising?

Share classes directly shape control, dilution, and investor rights, so the wrong structure can undermine governance and derail future fundraising.

Voting Power Distribution

Different share classes allocate voting rights differently. Ordinary shares usually grant one vote per share, while non‑voting shares confer no vote at all. Preference shares often carry restricted votes. When designing your UK fundraising share structure, map out how votes will be distributed among founders, investors and the option pool. Unequal voting can have long‑term governance implications, including board appointments and major corporate decisions.

Investor Control and Board Seats

Series A investors often negotiate rights to appoint directors. Preference shareholders may receive board seats or observer rights as part of their share class terms. Founders who wish to retain control can use super‑voting shares or maintain a majority of ordinary shares. However, super‑voting rights must be carefully drafted to remain SEIS/EIS‑compliant and not create an economic preference.

Dilution Mechanics

Issuing new shares reduces each existing shareholder’s percentage ownership. Complex preference stacks can amplify dilution by requiring that liquidation preferences be satisfied before ordinary shareholders receive any proceeds. Modelling different funding scenarios using cap table modelling tools helps founders understand how new rounds impact their equity. This modelling should include anti‑dilution provisions, option pools and any convertible instruments like Advance Subscription Agreements (ASA) or Convertible Loan Notes (CLN).

Long‑Term Effects on Future Rounds

Early decisions about share classes can influence valuation and investor appetite. Investors often shy away from companies with messy cap tables or hidden preferences. Layered preferences can create an overhang that depresses returns for ordinary shareholders and complicates secondary sales. Clean structures with one class of ordinary shares are easier to diligence and value.

Choosing the Right Share Class for Your Fundraising Stage

Your fundraising stage determines which share classes are viable, because SEIS/EIS constraints shift over time and later rounds demand different rights and protections.

Pre‑Seed (SEIS): Ordinary Shares Only

At the pre‑seed stage, startups typically rely on SEIS and raise relatively small sums. HMRC requires ordinary shares only to maintain eligibility. Avoid preference shares, redeemable shares or alphabet shares with preferential rights. Keep the cap table simple and use an option pool for team incentives.

Seed (EIS): Ordinary Shares With Simple Structure

The EIS stage allows for larger investments, but the share requirements remain the same: ordinary shares with no preferential rights. You can introduce alphabet shares to vary dividends, but ensure no class receives priority or fixed returns. Many founders also prepare for a larger option pool at this stage to attract senior hires.

Series A+: Introduction of Preference Shares

Once your company has grown beyond SEIS/EIS periods, you may issue preference shares to VC investors. Terms may include a 1× or 2× liquidation preference, dividends (often non‑cumulative) and anti‑dilution provisions. Ensure that existing shareholders understand how these preferences affect their returns. Use convertible instruments like ASAs or CLNs thoughtfully; they convert into shares at a discount and can affect valuations.

Hybrid or Complex Structures (Convertible, ASA)

Convertible loan notes and ASAs defer valuation by converting into shares at a future financing. They are not share classes but instruments that may convert into preference or ordinary shares later. While they can speed up funding, they add complexity to your cap table. Ensure your Articles of Association share classes allow for conversion and that investors understand the terms. SEIS/EIS rules may still apply if conversion happens within the qualifying period.

How Does Undo Capital Help Startups Issue the Correct Share Classes?

Undo Capital provides a modern platform for UK startups to manage equity, raise funds and stay compliant. According to the company’s site, it offers a modern‑era cap table management tool that lets companies view, track and manage equity in a few clicks. Its workflows mirror HMRC processes and Companies House record structures, ensuring every share issue and update is accurate, audit‑ready and regulation‑safe.

Key features include:

- Automated ordinary share issuance. Generate SEIS/EIS‑compliant share certificates and filings automatically.

- SEIS/EIS compliance tools. Apply for advance assurance, generate SEIS1/EIS1 compliance statements and track HMRC deadlines.

- Cap table management and modelling. Visualise ownership, model dilution, and simulate future rounds.

- ASA and subscription agreement generation. Create legally sound ASAs, subscription agreements and founder agreements using approved templates.

- Articles of Association analysis. Review your Articles to identify preferences and ensure compliance with SEIS/EIS rules.

- Data room and investor communications. Share documents securely with investors and manage soft commitments through a single platform.

Undo Capital acts as a one‑stop shop for SEIS/EIS rounds, funding rounds and ongoing equity management, helping founders avoid costly errors while maintaining a clean cap table.

FAQs

What share class is required for SEIS/EIS?

SEIS and EIS require ordinary shares that carry no preferential rights to dividends, assets or redemption. Limited non‑cumulative dividends are permitted, but cumulative or variable dividends and fixed returns are disallowed.

Can UK startups issue preference shares at pre‑seed?

No. To qualify for SEIS/EIS, you must issue only ordinary shares. Preference shares with fixed dividends or liquidation preferences will disqualify the round. Preference shares typically appear in Series A and later rounds.

What are alphabet shares?

Alphabet shares are different classes of ordinary shares (A, B, C, etc.) designed to vary dividend or voting rights between shareholders. They must still be ordinary shares for SEIS/EIS purposes and should not confer preferential economic rights.

Are non‑voting shares allowed under SEIS/EIS?

Non‑voting shares are allowed if they carry the same economic rights as voting shares. Any priority dividend or liquidation preference will make them non‑compliant.

How do founder shares work in the UK?

Founder shares are common shares issued to the founders at incorporation. They are usually low‑priced and may carry enhanced voting rights. They must avoid economic preferences if the company intends to issue SEIS/EIS shares later.

References

Disclosure Notice: This communication is issued by Undo Capital Limited (“Undo Capital”) and is provided strictly for informational purposes only. It contains general information and should not be relied upon as accounting, business, financial, investment, legal, tax, or other professional advice. Undo Capital is not regulated by the Financial Conduct Authority (FCA) and does not provide investment, financial, or tax advice. Our services are designed to assist startups and businesses with company formation, legal agreements, and funding-related documentation. Nothing in this communication constitutes, or should be construed as, a recommendation, offer, or solicitation to purchase or sell any security or financial instrument.

Participation in startups and early-stage enterprises involves significant risk. Such investments may be illiquid, may not generate dividends, may be subject to dilution, and may result in the total loss of invested capital. Any decisions or actions that may affect your business or personal interests should be taken only after seeking advice from suitably qualified professional advisors, and should form part of a balanced and diversified portfolio. This communication may contain links to third-party websites. The inclusion of such links does not imply endorsement, approval, investigation, or verification by Undo Capital. We accept no responsibility or liability for the content, accuracy, or use of information contained on any third-party websites.

Latest articles

%20Explained%20for%20UK%20Founders.jpg)

Share Incentive Plan (SIP) Explained for UK Founders

S431 Election Explained: What UK Founders Must Do When Issuing Shares to Employees