UK Investment Tax Reliefs Explained: EIS, SEIS & VCT Changes for 2026

- Bigger limits, bigger opportunities: From 6 April 2026, qualifying companies can have assets up to £30 million before and £35 million after a share issue, and can raise up to £10 million a year under the Enterprise Investment Scheme (EIS) (or £20 million for knowledge‑intensive companies). The lifetime cap doubles to £24 million, giving investors access to more established businesses and later‑stage rounds.

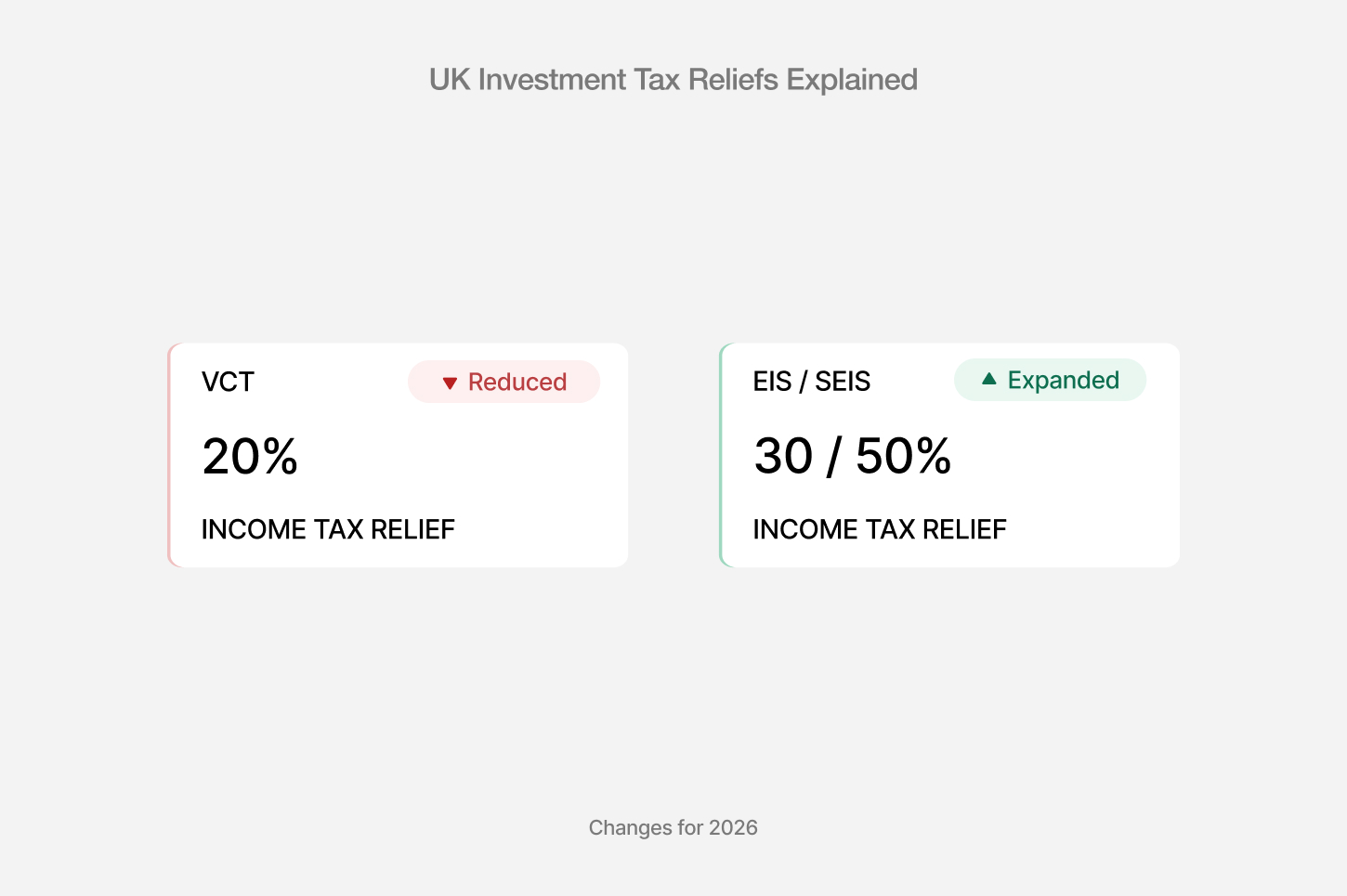

- VCT relief cut; EIS now stands out: Venture Capital Trust (VCT) income tax relief drops from 30% to 20% on new shares. The other benefits – tax‑free dividends and CGT‑free disposals – remain, but the reduced relief alters the risk–reward balance and makes EIS and Seed Enterprise Investment Scheme (SEIS) more compelling.

- SEIS unchanged but still generous: SEIS remains the “gold standard” for high‑risk early‑stage investing. Investors get 50% income tax relief on up to £200 k per year and can exempt half of their invested amount from other capital gains. No changes in April 2026 mean the scheme continues to offer outsized incentives for very young companies.

UK investors face a clear decision in 2026. The rules around investment tax relief have shifted. From 6 April 2026, what worked before no longer delivers the same return. The drop in VCT tax relief (from 30% to 20%) and the expansion of the Enterprise Investment Scheme have rebalanced the landscape. Many investors are now reassessing where to allocate capital.

Take a typical case. An investor who subscribed for venture capital trust shares before 6 April 2026 secured 30% income tax relief on a £100,000 investment. New VCT subscriptions from 6 April 2026 receive only 20% relief. That is a £10,000 gap per £100,000 invested.

The answer is not just to switch products. It is to understand how EIS investment tax relief, SEIS tax relief, and VCT incentives now interact. The changes create new opportunities. But they also increase the need for careful selection and structure.

This article breaks it down. You will learn how the 2026 reforms reshape EIS investments in the UK, how to compare the difference between EIS and VCT, and how to build a smarter, tax-efficient strategy going forward.

What Changed in UK Investment Tax Reliefs in April 2026

The reforms became effective for shares issued on or after 6 April 2026. They expand company eligibility while reducing relief for new VCT investors. This section covers the specifics.

Increased Company Limits and Investment Capacity

Under the expanded enterprise investment scheme, qualifying companies can now have gross assets up to £30 million immediately before issuing shares and £35 million immediately after. This is twice the previous threshold (previously £15 million/£16 million). The annual amount a company can raise under the EIS also doubles to £10 million (up from £5 million) or £20 million for knowledge‑intensive companies. The lifetime fundraising cap increases from £12 million to £24 million (and £40 million for knowledge‑intensive firms). These changes mean later‑stage scale‑ups can stay private longer and still offer tax‑advantaged equity.

The same higher limits apply to VCT‑qualifying companies. More businesses will therefore meet the criteria for both EIS and VCT investment, increasing deal flow and diversification for investors.

Important note for Northern Ireland investors: The new gross asset thresholds and fundraising limits described above apply to companies based in Great Britain only. Companies based in Northern Ireland remain subject to the previous limits, £15 million and £16 million for gross assets before and after a share issue, respectively, and the previous annual and lifetime fundraising caps. If you are investing in or through a Northern Ireland-based company, you should verify eligibility against the pre-2026 thresholds.

VCT Relief Reduction to 20%

From 6 April 2026, the income tax relief on new Venture Capital Trust subscriptions fell from 30% to 20%. Investors can claim this relief on up to £200k per tax year, and must hold the shares for at least five years to retain it. Dividends remain tax‑free, and disposal of VCT shares is exempt from capital gains tax. The government's rationale is that VCTs already provide tax‑free dividends, so a lower initial relief better matches the risk profile.

Bigger Funding Capacity

By raising the annual and lifetime fundraising limits and asset thresholds from 6 April 2026, the reforms aim to keep high‑growth companies in the UK for longer. Investors can now participate in Series B and C rounds through EIS and VCT rather than being restricted to seed and Series A. Knowledge‑intensive companies in sectors like deep tech and life sciences can raise £20 million per year under EIS, providing more headroom for R&D‑heavy businesses.

What Is EIS Tax Relief and Why It Still Leads the Market

The Enterprise Investment Scheme (EIS) remains the cornerstone of UK venture tax incentives. Its combination of income tax relief, capital gains tax (CGT) deferral, CGT exemption and loss relief provides powerful downside protection. This section explains how the scheme works, including the mechanics, limits and eligibility.

Income Tax Relief and Limits

EIS offers 30% income tax relief on investments up to £1 million per tax year. If you invest at least £1 million in knowledge‑intensive companies, the limit increases to £2 million. To claim the relief, you must be a UK taxpayer and buy new ordinary shares in a qualifying unquoted company. The shares must be held for at least three years. If you sell early, the relief is clawed back.

EIS tax relief explained: Suppose you invest £100,000 in an eligible company. You can reduce your income tax bill by £30,000 (30% of £100,000). If you invest £50,000, your relief is £15,000. The relief can be carried back to the previous tax year if you have not used your allowance.

CGT Deferral and Exemption

EIS investment allows you to defer capital gains from other asset disposals. You can reinvest the gain in EIS shares and postpone paying CGT until you sell the EIS shares. Additionally, if income tax relief has been claimed and not withdrawn, the gain on selling the EIS shares themselves is exempt from CGT.

EIS capital gains tax benefits in practice: If you sell a property for a £200,000 gain, you can reinvest that gain in EIS shares within the eligible window, up to one year before the disposal or up to three years after it, and defer the CGT. Later, when you sell the EIS shares (after at least three years), the deferred gain becomes chargeable. However, any new gain arising on the EIS shares themselves is exempt from CGT, provided income tax relief was claimed and not withdrawn. This flexibility helps investors manage both the timing of tax liabilities and cash flow across tax years.

Loss Relief Mechanics

If the company fails, loss relief allows investors to set losses against their income (not just other capital gains). For example, if a higher‑rate taxpayer (45% rate) invests £100,000, claims £30,000 income tax relief and then the company goes bust, the net cost is £70,000. They can offset 45% of the £70,000 loss (an additional £31,500) against their income. The effective cost becomes £38,500, meaning over 60% of the initial investment is covered by tax relief.

Other Investor Conditions

To qualify for EIS income tax relief, investors must not be connected to the company (no more than 30% shareholding or voting rights) and cannot be employed by it (except as an unpaid director). They must subscribe for new shares paid in full and hold them for at least three years.

Eligibility of Companies

EIS qualifying companies must carry on, or be preparing to carry on, a qualifying trade. Certain activities, such as banking, insurance, legal and accounting services, property development and farming, are excluded. For shares issued on or after 6 April 2026, companies must have gross assets not exceeding £30 million before and £35 million after the share issue and fewer than 250 employees (or 500 for knowledge‑intensive companies). Companies generally have seven years from their first commercial sale to raise EIS money. The funds raised must be used to grow or develop the business, not to acquire shares in other companies.

Maximum Company Fundraising and Investor Flexibility

From April 2026, the lifetime limit under EIS rises to £24 million. Annual fundraising increases to £10 million and £20 million for knowledge‑intensive companies. Investors can deploy capital across multiple EIS qualifying companies, building a diversified portfolio.

Why EIS Remains Attractive in 2026

The reduction in VCT relief makes EIS comparatively more generous. With 30% income tax relief, CGT deferral, CGT exemption and loss relief, EIS provides a powerful suite of incentives. The expanded company limits open the door to larger deals and later-stage rounds. Moreover, EIS shares may qualify for business relief (formerly business property relief) for inheritance tax, though the 2026 reforms cap 100% relief at £2.5 million of qualifying assets. For many investors, EIS offers the best blend of risk and reward when combined with professional due diligence.

SEIS Tax Relief: Higher Risk, Higher Incentives

The Seed Enterprise Investment Scheme (SEIS) targets very early‑stage startups. It provides 50% income tax relief on investments up to £200,000 per tax year. SEIS shares are exempt from CGT on disposal, and investors can set 50% of the amount invested against other capital gains, reducing taxable gains in the year of investment.

Early-Stage Focus and Qualifying Criteria

To be eligible, companies must have gross assets not exceeding £350,000 and fewer than 25 employees. The trade must be less than three years old, and the company must not have previously issued EIS or VCT shares. The maximum a company can raise under SEIS is £250,000.

Because SEIS covers smaller, riskier businesses, the relief is more generous. The 50% income tax relief provides a large buffer if the investment fails. Additionally, loss relief allows investors to offset losses against their income, further lowering their effective cost. However, the early‑stage nature of SEIS means higher failure rates and less liquidity compared with EIS.

Capital Gains Reinvestment Advantages

Investors can reinvest capital gains into SEIS shares and reduce up to 50% of the gain from tax. For example, if you sell shares and realise a £100,000 gain, reinvesting £100,000 into SEIS shares allows you to exempt £50,000 of that gain. Combined with the 50% income tax relief, the scheme offers substantial tax benefits for investors who can stomach the risk.

VCT Tax Relief Changes: What Investors Need to Know

Venture Capital Trusts (VCTs) are publicly listed investment vehicles that invest in diversified portfolios of small companies. They offer convenient access and built‑in diversification. However, the 2026 reforms reduce the income tax relief to 20%. Investors can claim the relief on up to £200,000 per tax year, provided they hold the shares for five years.

Core Features of VCTs

Even after the rate cut, VCTs still offer:

- Tax‑free dividends: dividends paid within the £200,000 annual limit are free of income tax.

- CGT‑free disposal: gains on the sale of VCT shares are not subject to capital gains tax.

- Portfolio diversification: VCTs must be listed on a recognised stock exchange, in practice, the London Stock Exchange. They must invest at least 80% of their assets in qualifying holdings and cannot allocate more than 15% to any single company."

- Expanded company limits: the same higher gross assets and fundraising limits that apply to EIS companies now apply to VCT investee companies.

Positioning VCTs Post‑2026

The reduction of VCT tax relief from 30% to 20% (effective 6 April 2026) has reduced the up‑front benefit and is prompting some investors to shift capital toward EIS or SEIS. VCTs still appeal to those seeking a dividend stream and preferring a managed, diversified portfolio. However, for investors comfortable constructing portfolios of EIS companies themselves (or using a platform like Undo Capital), the relative appeal of VCTs has diminished.

Example: A £50,000 VCT investment made before 6 April 2026 yielded £15,000 income tax relief. From 6 April 2026, a £50,000 new VCT subscription yields only £10,000 relief, a £5,000 reduction. For high‑rate taxpayers, that difference may tip the balance toward EIS investments."

EIS vs SEIS vs VCT: Key Differences for Investors

Below is a comparison of the three schemes. The table distils the features, limits and risk considerations.

How to Read the Table

- Income tax relief: Both EIS and SEIS provide stronger up‑front relief than VCTs (as of April 2026). EIS sits at 30%, SEIS at 50%, and VCT at 20% (down from 30% pre-April 2026). EIS income tax relief and SEIS income tax relief rates remain unchanged from their original scheme design; the change was to VCT relief only.

- CGT benefits: EIS and SEIS offer CGT exemption and, in EIS, deferral. VCTs provide tax‑free dividends and CGT‑free disposal, but no deferral or loss relief.

- Investment limits: EIS allows much larger investments, while SEIS is capped at £200 k. VCT investments are limited to £200 k per year, but investors can allocate across many companies.

- Risk: SEIS invests in nascent businesses; EIS covers early‑ to growth‑stage companies; VCTs deliver diversification but at a lower initial relief. Understanding the difference between SEIS and EIS and the difference between EIS and VCT helps investors allocate appropriately.

What These Changes Mean for Investors in 2026

These shifts are not incremental; they have changed how capital flows, how risk is priced, and how investors must now structure portfolios from 2026 onwards.

Greater Diversification and Later‑Stage Access

The expanded company limits widen the investable universe. More companies will meet the EIS and VCT criteria, enabling investors to build diversified portfolios across sectors and stages. Access to later‑stage rounds (Series B/C) via EIS reduces reliance on public markets for growth capital. Investors who previously reached the lifetime cap can now reinvest, thanks to the £24 million lifetime limit.

Relative Attractiveness of EIS and SEIS

The VCT tax relief cut to 20% (from 30%) has diminished VCT's comparative edge. EIS remains the workhorse, offering 30% income tax relief, CGT deferral, CGT exemption and loss relief. SEIS retains its 50% income tax relief and remains the best option for those willing to back very young startups. Investors should now compare the tax benefits of EIS (30%) with the reduced VCT benefit (20%) and decide whether the diversification of VCTs outweighs the lower upfront relief, or whether they can tolerate the extra due diligence of single‑company EIS investments.

EIS-Qualifying Companies Broaden

With gross assets up to £30/35 million and higher employee caps (250/500), the number of EIS qualifying companies increases. This opens opportunities in capital‑intensive sectors like biotechnology, advanced manufacturing and clean energy. Yet the trade exclusion rules remain; businesses in financial services, property development and farming still do not qualify.

Change in Inheritance Tax Treatment

From April 2026, business relief (formerly business property relief) is capped at £2.5 million per individual. Any value above that receives 50% relief. This affects high‑net‑worth individuals who have used EIS or SEIS to mitigate inheritance tax and may require them to re-evaluate estate planning. However, the relief still makes EIS investments attractive for amounts up to £2.5 million.

Rebalancing Toward Knowledge‑Intensive Companies

From 6 April 2026, the EIS maximum investment for knowledge‑intensive companies rises to £20 million annually and £40 million over the company's lifetime. These businesses often operate in research-heavy fields and require substantial capital. Investors seeking exposure to deep‑tech or life sciences may prioritise knowledge‑intensive EIS opportunities.

The Planning Window: April 2026 and Beyond

The opportunity to secure 30% VCT relief closed on 5 April 2026. From 6 April 2026 onwards, new VCT subscriptions receive 20% income tax relief instead. The difference between EIS and VCT is now stark. For example, a higher‑rate taxpayer who invested £200,000 in VCTs before 6 April 2026 secured £60,000 relief. New VCT subscriptions from 6 April 2026 yield only £40,000 relief—a £20,000 reduction. Investors with existing VCT portfolios should review whether to reinvest dividends (which remain tax‑free) or allocate future contributions to EIS/SEIS, which continue to offer stronger upfront relief.

How to Invest in EIS Opportunities in the UK

Investing in EIS (and SEIS) requires more hands‑on effort than purchasing VCT shares. But with the right guidance, investors can build a tailored portfolio that maximises tax efficiency. Here is a practical roadmap.

- Identify qualifying deals. Use specialist platforms such as Undo Capital to access vetted EIS investments in the UK. The platform curates opportunities across sectors and stages, ensuring companies meet EIS criteria. Investors can filter by industry, stage and knowledge‑intensive status, increasing the chance of diversification.

- Perform due diligence. Assess the company’s business model, team, traction and financial projections. Check that the company has EIS advance assurance from HMRC or intends to obtain it. Examine whether the company fits within your risk tolerance.

- Allocate across multiple companies. To mitigate risk, spread your EIS investment tax relief across several ventures. Platforms like Undo Capital make it easy to manage allocations, monitor performance and generate the necessary compliance paperwork.

- Obtain compliance certificates. After investing, the company (or platform) must issue an EIS3 certificate. This document is required to claim your EIS scheme income tax relief on your self‑assessment tax return.

- Claim the relief. Use your EIS3 certificate to claim income tax relief. You can carry relief back to the previous tax year if you haven’t used your allowance.

- Monitor holding period and conditions. Ensure you hold the shares for at least three years. If the company ceases to qualify (for example, by changing its trade), your relief may be withdrawn.

By following these steps, investors can harness investment tax relief while supporting innovative British businesses. Partnering with a specialist platform provides access to quality deals and simplifies compliance.

By understanding the tax benefits of EIS, SEIS and VCTs and by acting before and after April 2026, investors can optimise their tax position while supporting British innovation. The changes herald a scale‑up era where high‑quality deals demand both knowledge and agility. Explore curated EIS opportunities today to position your portfolio for the next decade of UK growth.

FAQs

What is EIS tax relief?

EIS tax relief is a UK income tax reduction equal to 30% of the amount invested in qualifying shares (up to £1 million, or £2 million for knowledge‑intensive companies). Investors must hold the shares for three years and meet various eligibility conditions.

How does EIS reduce capital gains tax?

EIS offers two CGT benefits: you can defer capital gains by reinvesting the gain in EIS shares, and you enjoy a CGT exemption on the EIS shares themselves. When the EIS shares are sold (after the three‑year holding period), the deferred gain becomes chargeable.

What is the difference between SEIS and EIS?

SEIS targets very early‑stage startups, offering 50% income tax relief on investments up to £200,000 and allowing investors to exempt half of reinvested gains. EIS covers slightly later‑stage companies, providing 30% income tax relief on up to £1 m (£2 m for knowledge‑intensive) and allowing capital gains tax deferral and loss relief.

Is VCT still worth it in 2026?

VCTs still offer tax‑free dividends and CGT‑free disposals, but the income tax relief on new subscriptions has fallen to 20% (from 30%). For investors seeking diversification and regular dividends, VCTs may still be attractive. However, if you prioritise larger upfront relief and can tolerate single‑company risk, investing in EIS or SEIS now provides comparatively better tax benefits.

What are the risks of EIS and SEIS investments?

Investing in unquoted early‑stage companies carries a high risk of failure and illiquidity. SEIS investments are particularly high-risk because companies are less than 3 years old and can raise only up to £250k. EIS investments involve medium risk: companies can be early or growth stage, and must be held for three years. Loss relief mitigates risk but does not eliminate it. Always diversify and seek professional advice.

References

- EIS, SEIS, VCT and UK investment tax reliefs explained - Saffery

- Autumn Budget 2025: A summary - House of Commons Library

- Venture Capital Trusts, Enterprise Investment Scheme investment limit increase and restructure - GOV.UK

- HS297 Capital Gains Tax and Enterprise Investment Scheme (2024) - GOV.UK

- Tax relief for investors using venture capital schemes - GOV.UK

- Inheritance tax reliefs threshold to rise to £2.5m for farmers and businesses - GOV.UK

Disclosure Notice: This communication is issued by Undo Capital Limited (“Undo Capital”) and is provided strictly for informational purposes only. It contains general information and should not be relied upon as accounting, business, financial, investment, legal, tax, or other professional advice. Undo Capital is not regulated by the Financial Conduct Authority (FCA) and does not provide investment, financial, or tax advice. Our services are designed to assist startups and businesses with company formation, legal agreements, and funding-related documentation. Nothing in this communication constitutes, or should be construed as, a recommendation, offer, or solicitation to purchase or sell any security or financial instrument.

Participation in startups and early-stage enterprises involves significant risk. Such investments may be illiquid, may not generate dividends, may be subject to dilution, and may result in the total loss of invested capital. Any decisions or actions that may affect your business or personal interests should be taken only after seeking advice from suitably qualified professional advisors, and should form part of a balanced and diversified portfolio. This communication may contain links to third-party websites. The inclusion of such links does not imply endorsement, approval, investigation, or verification by Undo Capital. We accept no responsibility or liability for the content, accuracy, or use of information contained on any third-party websites.

Latest articles

Pre-Seed Funding UK: What It Is, How Much to Raise, and How to Find Investors in 2026

How to Set Up a Virtual Data Room for Startup Fundraising (2026 Guide)