Share Certificate UK: What It Is, What It Must Show, and How to Issue One

- Know the document – A share certificate is the legal proof of your ownership. It lists your company’s name, your name, the number of shares and their class. It is also known as a shareholder certificate or shares certificate, and it must be issued within two months after allotment or transfer.

- Keep your register in sync – Share certificates aren’t sent to Companies House. The register of members is the official record of ownership. You must update this register and file Form SH01 with Companies House within one month of allotting new shares.

- Follow the process – To issue or sell shares, approve them in a board resolution, update your internal records, prepare the share certificate using the right template, sign it, and send it to the shareholder. When transferring, complete a Stock Transfer Form J30, pay 0.5% Stamp Duty on consideration over £1,000, and cancel the old certificate.

A founder closes a funding round and celebrates, until their new investor asks, “Where’s my share certificate?” Many first‑time founders don’t realise that a share certificate isn’t just a formality. It is a legal document that proves who owns what. If you fail to issue one on time or leave out crucial details, you risk fines, investor disputes, and delays in future funding rounds.

This guide explains what a share certificate is, what it must show, how to issue it and how to transfer shares with it, using plain English and practical examples. The goal is to answer what a share certificate is and show how you comply, not just tell you what to do.

What is a share certificate?

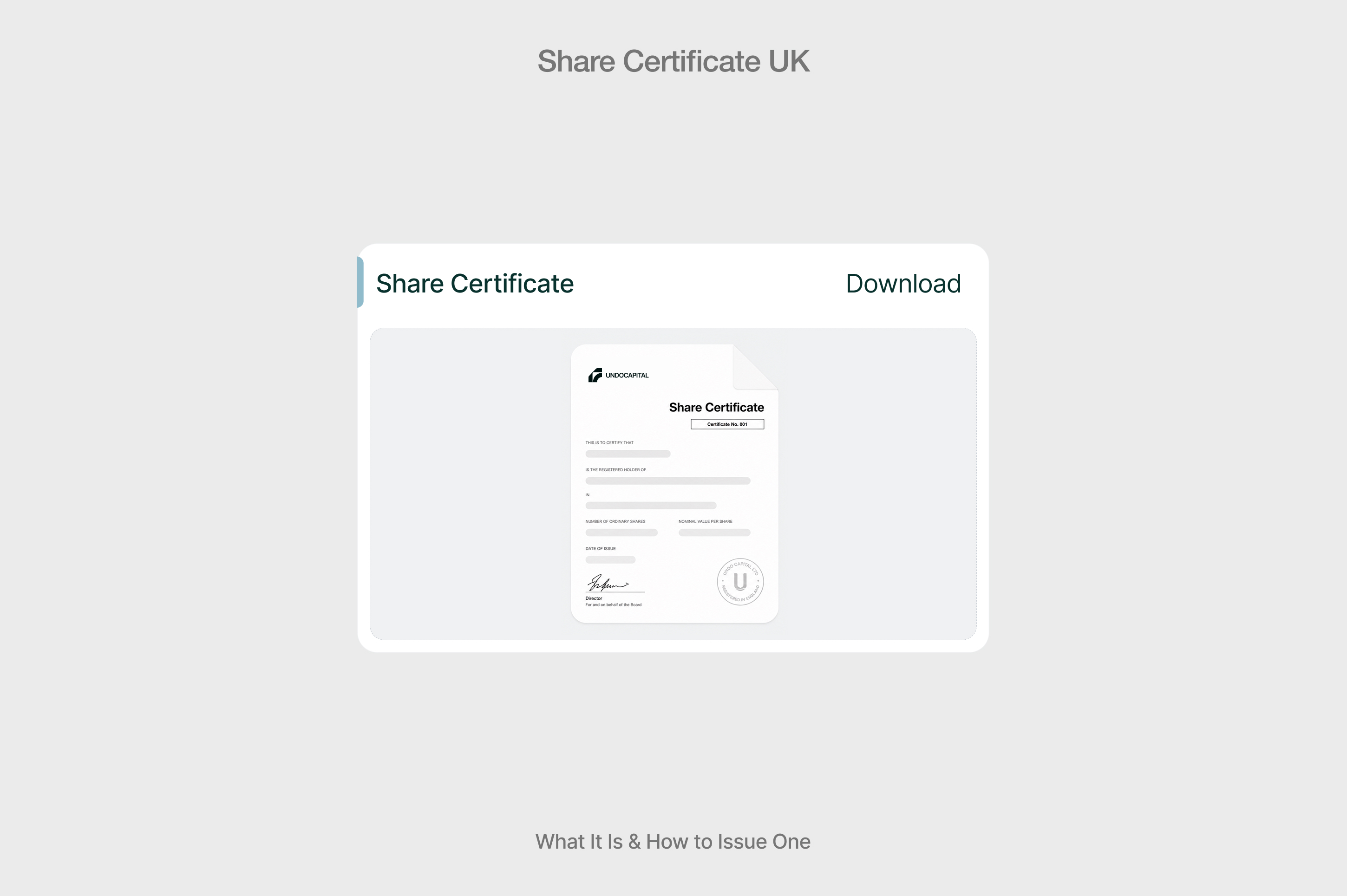

A share certificate (sometimes called a shareholder certificate, shares certificate or, in US terminology, stock certificate) is the document that shows who owns shares in a UK company. Section 768 of the Companies Act 2006 says that a share certificate under the company’s seal is prima facie evidence of title to the shares. In other words, the certificate is the proof a shareholder can use in court or during due diligence to demonstrate they own those shares. The document is usually one page long. It notes the shareholder’s name, the number and class of shares held, the nominal value and the date of issue. It is not filed at Companies House and is separate from the register of members.

A share certificate is different from a stock certificate issued for US companies. In the UK, the certificate is primarily used for private companies. Public companies listed on exchanges issue electronic statements and CREST accounts, while physical certificates are rare. Regardless of format, UK law requires companies to deliver a share certificate to the shareholder within two months of allotting or transferring shares. Failure to do so is an offence and can lead to fines for company officers.

What must a share certificate include? (UK legal requirements)

To comply with the Companies Act and model articles, your share certificates must include all the information investors expect. Section 769 of the Companies Act 2006 requires companies to have share certificates ready for delivery within two months of allotting shares. Section 776 imposes the same two-month duty when shares are transferred.

Guidance from law firms and company secretarial experts describes the minimum details:

- Company name and registration number – The legal name and Companies House number appear at the top.

- Certificate number – Each certificate should have a unique sequential number.

- Shareholder’s name and address – The person or entity holding the shares.

- Number of shares and class – For example, 10 ordinary shares or 1 preference share; include the nominal value (e.g., £0.01 per share).

- Amount paid and unpaid – Show how much has been paid on the shares and any unpaid amount (rare in modern startups).

- Date of issue – The day the certificate was created.

- Authorised signatures – Either two directors, one director and a company secretary or one director and a witness.

- Company seal (optional) – Many modern companies use authorised signatures instead of a seal.

These requirements come directly from the Companies Act 2006 and model articles. Section 769 states that failing to issue certificates within the two‑month window is an offence, and Section 768 makes the certificate prima facie evidence of title. Seeds of non‑compliance include using duplicate certificate numbers, issuing unsigned certificates or forgetting to cancel old certificates when shares are transferred.

Share certificate vs. Companies House: what’s the difference?

Many founders assume that sending documents to Companies House automatically proves ownership. That’s a misconception. Share certificates are not filed at Companies House. The official proof of ownership is the register of members, sometimes kept internally or, after November 2025, kept by Companies House. The register must record each member’s name, service address, date of registration, number and class of shares, certificate numbers and amounts paid/unpaid. It must also record transfers – including the date, transferor and transferee – and the date a member ceases to hold shares.

The register is the statutory book that shows who owns the company at any point. Companies House collects summary information through the confirmation statement and Form SH01, but it does not hold individual certificates. Under the Economic Crime and Under the Economic Crime and Corporate Transparency Act 2023, several changes came into force from 18 November 2025, including mandatory identity verification for directors and PSCs and the abolition of certain internal registers (directors, secretaries, and PSCs). However, the register of members is not affected in the same way: companies must still maintain their own internal register of members.

In fact, the previous option to elect to hold member information on the central Companies House register has been abolished. What did change from November 2025 is that companies must now provide a one-off full shareholder list, including full names of all members, as part of their next confirmation statement filing. Otherwise, you must maintain it yourself. Failing to update the register within two months of an allotment or transfer can be a criminal offence.

In practice, you issue the share certificate directly to the shareholder, update your internal register and file any required returns (such as Form SH01) with Companies House. No copy of the certificate goes to the registrar. This is why investors often ask to see both the certificate and the register during due diligence: one proves you followed the law; the other proves the investor’s stake.

What are certificate shares? Types explained

A share certificate can relate to different types of shares, each carrying distinct rights. Understanding classes helps you design cap tables and issue certificates correctly:

- Ordinary shares – The most common class in startups. Each ordinary share typically carries one vote per share, equal dividend rights and equal rights to capital on winding up. They represent most of the equity in early‑stage companies.

- Preference shares – These shares carry preferential rights. HMRC’s manuals note that preference shareholders often receive a fixed dividend before ordinary shareholders and may have limited voting rights. Their rights to capital may also take precedence in a liquidation.

- Growth shares – Popular with startups seeking to incentivise employees and advisors. A growth share allows the holder to benefit only from company value above a threshold (the “hurdle”), ring‑fencing existing shareholders’ equity. A law‑firm guide explains that growth shares allow employees, family members or advisors to participate in future growth beyond a fixed valuation; the existing shareholders’ equity is protected. This class is often used when EMI or other HMRC‑approved options aren’t available. Growth shares usually carry limited voting rights and no dividends until the hurdle is met.

- Deferred or non‑voting shares – Sometimes used to hold founder equity with restrictions or for investors who don’t need votes.

Each share class may have its own share certificate. When you issue multiple classes on the same day, you must issue a separate certificate for each share class. Section 24 of the model articles for private companies limited by shares states that no certificate may be issued in respect of shares of more than one class. Note that share options (EMI or unapproved options) do not create shares until exercised. Option holders do not receive a share certificate until the option is exercised and shares are issued.

How to issue a share certificate in the UK (step‑by‑step)

Issuing a share certificate is straightforward when you follow the right steps. Here is a practical, founder‑friendly process:

- Allot the shares through a board resolution. Before issuing new shares, directors must have the authority to allot under sections 550 or 551 of the Companies Act. For most private companies with one share class, directors can allot without shareholder approval, but check your articles. For companies incorporated before 2006 or those with multiple classes, you may need an ordinary resolution of shareholders. Document the resolution specifying the class, number and price. If pre‑emption rights exist, issue a special resolution to disapply them before allotting.

- Collect payment and update the register of members. Shares must be fully paid unless your articles permit partly paid shares. UK law mandates payment on allotment. Record the allottee’s details in your register of members: name, address, number and class of shares, certificate number, amount paid and the date of entry. Make sure to cross‑reference the entry with your statutory registers of allotments and transfers.

- Prepare the share certificate. Use a shareholder certificate sample or template. Include all the details listed above: company name, registration number, certificate number, shareholder details, share class, number, nominal value, amount paid, date of issue and authorised signatures. Using a software platform like Undo Capital’s cap table tool automatically generates compliant certificates and logs the certificate number.

- Sign and issue within two months. Have two directors sign; if you only have one director, add the company secretary or a witness. Date the certificate and send a copy (paper or digital) to the shareholder. The Companies Act allows up to two months from the allotment date; however, investors appreciate promptness. For example, if you allot shares on 1 February, issue the certificate by 31 March.

- File Form SH01 with Companies House. A return of allotment (Form SH01) must be filed within one month of the allotment date, as required by Section 555 of the Companies Act 2006. SH01 captures the number of shares, nominal value, share premium and rights attached. Failure to file on time is a criminal offence and can lead to fines. After filing, update your confirmation statement and plan for the new requirement from November 2025 to include the full list of shareholders.

- Communicate with stakeholders. Send investors the certificate and, if applicable, share their new ownership in your cap table. Provide board minutes and the SH01 filing confirmation. Using Undo Capital’s cap table management software ensures your internal records remain consistent with the public register.

Example costs

Issuing shares involves minimal official fees but may include professional costs. Filing a Form SH01 online with Companies House is currently free of charge. Paper submissions carry a small fee; check the current Companies House fee schedule to confirm the latest figure. Professional costs for legal advice and preparing subscription agreements typically range from £500 to £800 for a straightforward allotment. Some investors insist on legal review of subscription agreements, which can increase cost. These figures illustrate why automating the process can save you money.

How to sell shares with a share certificate

Transferring shares is different from allotment. When you sell or transfer existing shares, you move ownership from the seller to the buyer without creating new shares. Here is how to handle selling shares with a share certificate:

- Check your articles and shareholder agreements. Private companies often have pre‑emption rights (the right of first refusal) requiring existing shareholders to approve the transfer. Obtain board approval and, if necessary, a special resolution disapplying pre‑emption rights.

- Complete a Stock Transfer Form (J30). For fully paid shares, use Form J30; for partly paid shares, use Form J10. The seller fills in the quantity, class and nominal value, buyer’s name and address, seller’s name and address, and the consideration. You must send the form to HMRC if the consideration exceeds £1,000.

- Pay Stamp Duty if applicable. If the transfer value is over £1,000, you pay 0.5% duty, rounded up to the nearest £5. For example, on a £5,000 sale, you pay 0.5% (£25). HMRC requires you to email the completed Stock Transfer Form to stampdutymailbox@hmrc.gov.uk and pay the Stamp Duty within 30 days of signing. Since March 2020, HMRC no longer accepts posted stock transfer forms as standard; email is the required submission method. If you complete certificate 1 or certificate 2 on the back of the form (for transfers under £1,000 or exempt transfers), you usually don’t need to pay any duty.

- Surrender and cancel the old certificate. The seller returns the original share certificate. Once the transfer is approved, cancel the old certificate and issue a new one to the buyer. Keep the cancelled certificate in your records for auditing and evidence.

- Update registers and notify the buyer. Record the transfer in your register of members, noting the transferor, transferee, date and certificate number. Issue the new share certificate within two months. For transparency, update your confirmation statement at the next filing.

- Example costs and timing. Stamp Duty of 0.5 % applies only on transfers over £1,000. Processing fees for company secretarial services range from £100 to £300, and legal advice may add more. Transfers generally complete within one to two weeks once board approval and HMRC stamping are done.

Selling shares with a share certificate isn’t just paperwork; it protects both parties. Without a proper transfer instrument and updated register, the buyer may not be recognised as a shareholder and cannot exercise rights or receive dividends.

Do digital share certificates count in the UK?

Yes. Electronic share certificates are valid and increasingly common. Sections 769 and 776 of the Companies Act require that share certificates be ready for delivery within two months of allotment and transfer, respectively, but neither mandates paper. Modern platforms like Undo Capital generate PDF certificates with electronic signatures. Guidance on electronic signatures under the Electronic Communications Act 2000 and the UK eIDAS Regulation states that a signature cannot be denied legal effect solely because it is in electronic form. Furthermore, digital certificates are recognised if they are signed by authorised persons and clearly show the shareholder’s details and share class. They reduce costs, eliminate printing and mailing delays, and integrate with cap table software to maintain accurate registers.

While electronic certificates are valid, you must still keep your register up to date and follow the two‑month issuance window. If you issue digital certificates, ensure that the electronic signature process is secure and that you can reproduce the certificate on demand. Undo Capital’s digital share issuance tool automates this process and stores signed certificates in a secure data room.

FAQs

What is a share certificate, and why do you need one?

A share certificate is a formal document proving that a named individual or entity owns a specific number and class of shares in your company. It serves as evidence of title and must be delivered within two months of allotting or transferring shares. Without it, investors may question the legitimacy of their holdings, and company officers could be fined for non‑compliance.

Is a share certificate the same as a shareholder certificate?

Yes. In UK law, the terms share certificate and shareholder certificate refer to the same document. In the US, the equivalent is called a stock certificate. Regardless of terminology, the document must contain the company name, registration number, shareholder details, share class, nominal value and authorised signatures.

Do share certificates need to be registered at Companies House?

No. Share certificates are not filed at Companies House. Instead, you must update your internal register of members and file a Form SH01 within one month of allotting new shares. The register is the definitive record of ownership, and Companies House only receives summary information through confirmation statements and SH01 filings.

How long does a company have to issue a share certificate?

Under Section 769 of the Companies Act 2006, you must issue a share certificate within two months of the date on which shares are allotted or transferred. If you allot shares on 1 June, the certificate must be issued by 31 July. Failure to comply is a criminal offence.

Can I sell my shares without a share certificate?

If you have lost your certificate, you can still transfer shares, but you will need to sign a letter of indemnity. The company will cancel the old certificate and issue a new one to the buyer. You must still complete a Stock Transfer Form, pay any Stamp Duty due and update the register. Without a certificate or indemnity, the company may refuse to register the transfer.

References

Disclosure Notice: This communication is issued by Undo Capital Limited (“Undo Capital”) and is provided strictly for informational purposes only. It contains general information and should not be relied upon as accounting, business, financial, investment, legal, tax, or other professional advice. Undo Capital is not regulated by the Financial Conduct Authority (FCA) and does not provide investment, financial, or tax advice. Our services are designed to assist startups and businesses with company formation, legal agreements, and funding-related documentation. Nothing in this communication constitutes, or should be construed as, a recommendation, offer, or solicitation to purchase or sell any security or financial instrument.

Participation in startups and early-stage enterprises involves significant risk. Such investments may be illiquid, may not generate dividends, may be subject to dilution, and may result in the total loss of invested capital. Any decisions or actions that may affect your business or personal interests should be taken only after seeking advice from suitably qualified professional advisors, and should form part of a balanced and diversified portfolio. This communication may contain links to third-party websites. The inclusion of such links does not imply endorsement, approval, investigation, or verification by Undo Capital. We accept no responsibility or liability for the content, accuracy, or use of information contained on any third-party websites.

Latest articles

Pre-Seed Funding UK: What It Is, How Much to Raise, and How to Find Investors in 2026

How to Set Up a Virtual Data Room for Startup Fundraising (2026 Guide)